The central government debt ratio in the advanced economies has reached a 200-year high watermark. Other levels of government debt, unfunded pension and health care liabilities, and a huge external debt stocks add to scale and complexity of the problem. A historical analysis of Carmen Reinhart and Kenneth Rogoff suggests that developed countries, like emerging markets, are prone to taking recourse to aggressive financial repression and even debt restructuring.

“Financial and Sovereign Debt Crises: Some Lessons Learned and Those Forgotten”

Carmen M. Reinhart and Kenneth S. Rogoff

IMF Working Paper, 13-266, December 2013

http://www.imf.org/external/pubs/ft/wp/2013/wp13266.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

“[The prevailing official view] is that debt sustainability [in developed countries] can be achieved through a mix of austerity, forbearance and growth. The claim is that advanced countries do not need to resort to the standard toolkit of emerging markets, including debt restructurings and conversions, higher inflation, capital controls and other forms of financial repression…this claim is at odds with the historical track record of most advanced economies, where debt restructuring or conversions, financial repression, and a tolerance for higher inflation… were an integral part of the resolution of significant past debt overhangs.”

Excessive public debt in developed countries: The main historical lessons

Lesson 1: Developed countries have a poor record in crisis prevention

“On prevention versus crisis management…we have done better at the latter than the former. It is doubtful that this will change as memories of the crisis fade and financial market participants and their regulators become complacent.”

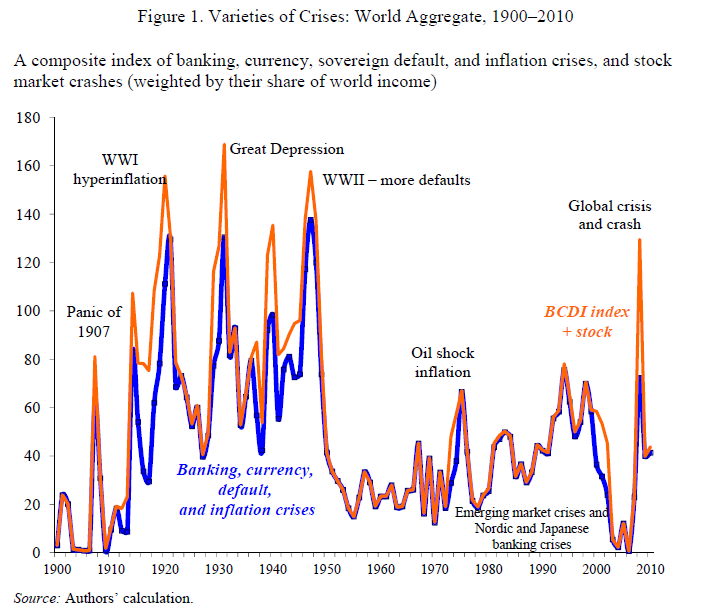

“Figure 1 presents a composite index of banking, currency, sovereign default, and inflation crises, and stock market crashes. Countries are weighted by their share of world income, so advanced countries carry proportionately higher weights. The figure…shows that the ‘financial repression’ period, 1945–1979 in particular, has markedly fewer crises than earlier or subsequently… ‘Financial repression’ includes directed lending to government by captive domestic audiences (such as pension funds), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and generally a tighter connection between government and banks.”

Lesson 2: Markets underestimate scale and complexity of debt problems

“The magnitude of the overall debt problem facing advanced economies today is difficult to overstate. The mix of an aging society, an expanding social welfare state, and stagnant population growth would be difficult in the best of circumstances. This burden has been significantly compounded by huge increases in government debt in the wake of the crisis.”

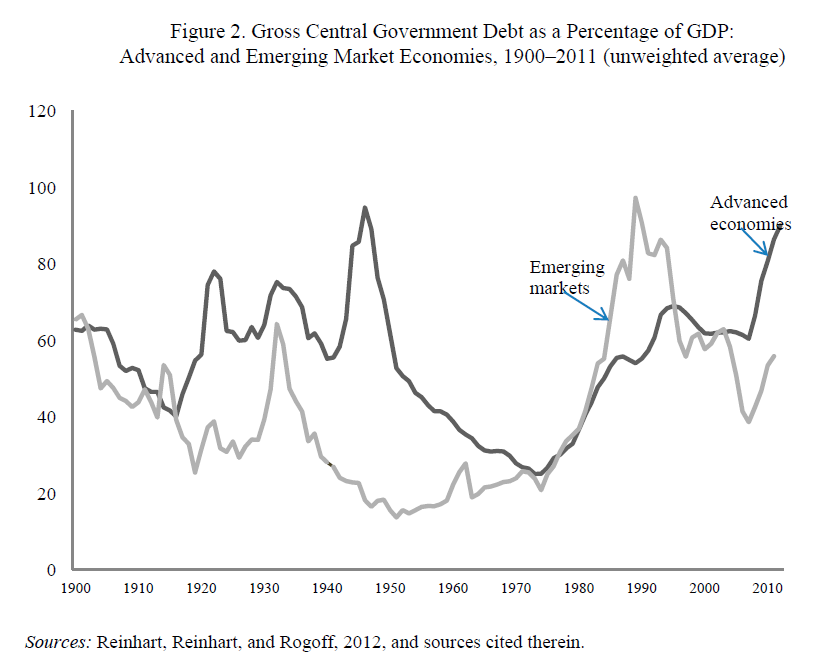

“Going back to 1800, the current level of central government debt in advanced economies is approaching a two-century high-water mark. Broader debt measures that include state and local liabilities…would almost surely make the present public debt burden seem even larger… Including the liability side of old-age pensions and medical benefits would make the overall debt picture much worse today relative to earlier periods.”

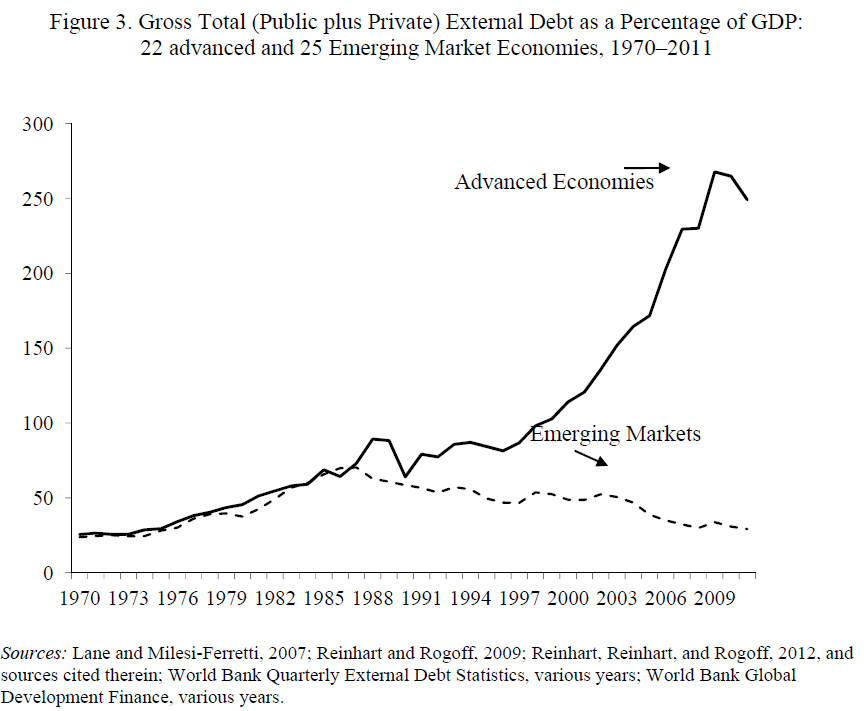

“External debt is another important marker of overall vulnerability… total external debt is an important indicator because the boundaries between public and private debt can become blurred in a crisis. External private debt (particularly but not exclusively that of banks) is one of the forms of ‘hidden debt’ that emerge out of the woodwork in a crisis.”

Lesson 3: Developed and emerging countries are not that different in respect to debt resolution

“There are essentially five ways to reduce large debt-to-GDP ratios. Most historical episodes have involved some combination of these…(1) economic growth(2) fiscal adjustment [or] austerity (3) explicit default or restructuring, (4) inflation surprise, (5) a steady dose of financial repression accompanied by a steady dose of inflation.”

“The first on the list is relatively rare and the rest are difficult and unpopular. Recent policy discussion has tended to forget options (3) and (5), arguing that advanced countries do not behave that way. In fact, option (5) was used extensively by advanced countries to deal with post–World War II debt and option (3) was common enough before World War II.”

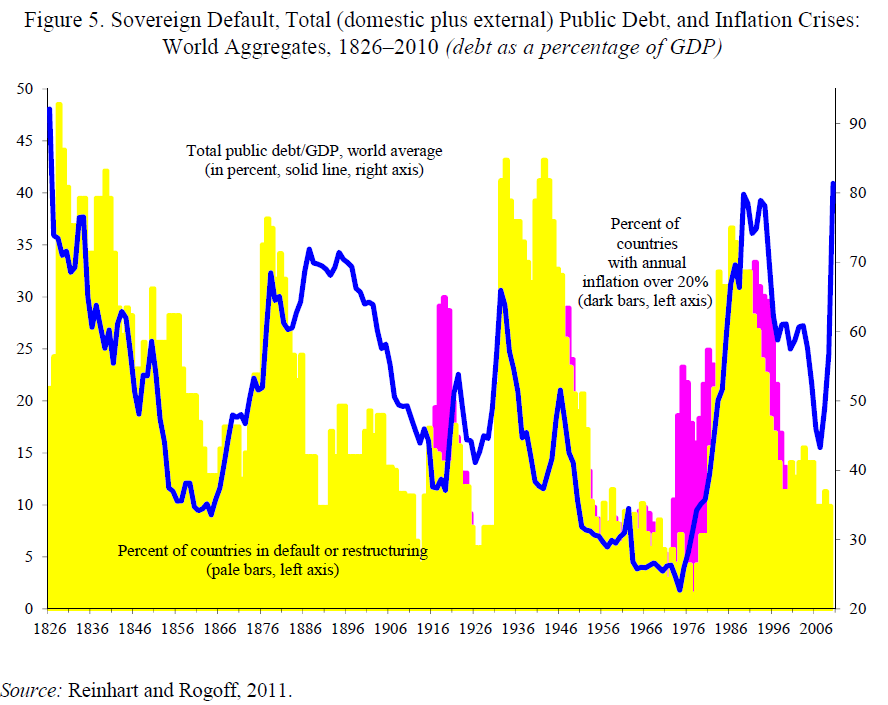

“Historically, periods of high government debt such as the current one have led to marked increases in debt restructurings, as Figure 5 illustrates. The figure plots GDP-weighted central government debt against the percentage of countries experiencing inflation higher than 20 percent as well as the share of countries engaged in debt restructuring, from 1826 through 2010.”

“13 of 21 advanced economies had at least one credit event involving the sovereign. A number of countries had multiple debt crises and an even larger number…had, especially during the 1930s, wholesale private defaults, as evidenced by bank failures and nonfinancial corporate bankruptcies.”

Lesson 4: Mind particularly financial repression

“Following World War II (when explicit defaults were limited to the losing side), financial repression via negative real interest rates reduced debt to the tune of 2 to 4 percent a year for the United States, and for the United Kingdom for the years with negative real interest rates. For Italy and Australia, with their higher inflation rates, debt reduction from the financial repression ‘tax’ was on a larger scale and closer to 5 percent per year.”