Hagendorff and Vallascas argue that the risk weights used to calculate banks’ capital adequacy fall significantly short of true portfolio risks. Capital arbitrage may have undermined Basel II capital regulation and could do the same for Basel III in the future.

“Bank capital requirements: Risk weights you cannot trust and the implications for Basel III”, Jens Hagendorff and Francesco Vallascas, 16 December 2013, on VOX

http://www.voxeu.org/article/basel-risk-weights-can-t-be-trusted

“The Risk Sensitivity of Capital Requirements: Evidence from an International Sample of Large Banks.”, Jens Hagendorff and Francesco Vallascas, Review of Finance, 17: 1947–1988.

Public link to related working paper: http://www.fma.org/Istanbul/Papers/capitalrequirements.pdf

A useful summary presentation: http://www.chicagofed.org/digital_assets/others/events/2012/bsc/vallascas_hagendorff_050912.pdf

The below are excerpts from the post and papers. Cursive text and emphasis has been added.

The issue at stake

“The financial crisis that started in 2007 illustrates that capital-adequacy rules have failed to ensure that banks’ capital holdings are in line with the riskiness of their assets. This is true despite numerous refinements and revisions over the last two decades.”

“The Basel Accord of 1988 introduced minimum capital standards as a fixed proportion of the risk exposure of a bank, as measured by risk-weighted assets. In most countries, the minimum capital requirement is 8% of risk-weighted assets… [Risk-weighted assets denote] the weighted sum of various on- and off-balance sheet exposures…[which] has become more comprehensive over time to include market risk and operational risk… Underlying Basel is the notion that the risk weights assigned to each asset class reflect the associated economic risks. Thus, a key question is whether this regulatory measure of bank portfolio risk is reflective of the true portfolio risk of a bank. If not, banks will try to game the system by investing in risky assets which maximize returns while reducing capital requirements.”

Evidence of inappropriate risk weights

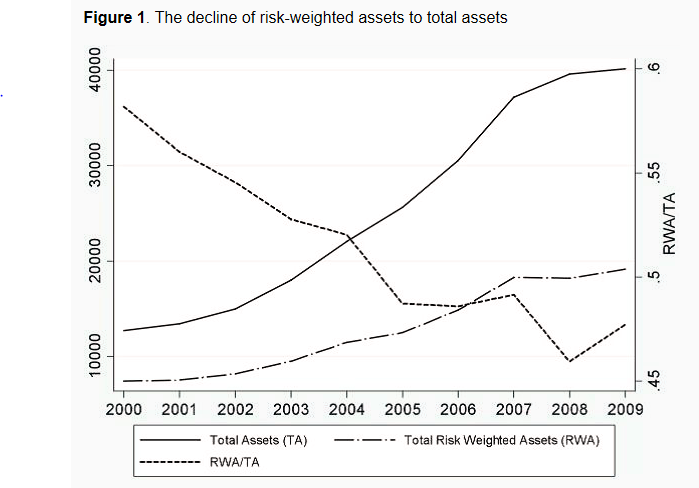

“Banks’ ability to game the system is nicely illustrated by [the graph below]. The graph shows the value of total assets, risk-weighted assets, and the proportion of risk-weighted assets to total assets of the world’s largest 124 banks. The proportion of risk-weighted assets to total assets has been falling steadily since 2000. One way of interpreting this is that banks have become progressively less risky over time. A different interpretation is that banks have increasingly gamed the Basel rules, resulting in lower risk-weighted assets – and thus lower capital requirements – but probably no less risk.”

“We examine the risk sensitivity of capital requirements for an international sample of large banks between 2000 and 2010. We demonstrate that capital requirements are only loosely related to a market measure of the portfolio risk of banks. Owing to this weak risk calibration, even pronounced increases in portfolio risk generate almost negligible increases in capital requirements. To illustrate this, we show that when the market measure of portfolio risk increases nearly threefold (from 2.1% to 6.2%), the average bank in our sample faces additional capital requirements of 0.78 percentage points (assuming capital requirements of 8% of risk-weighted assets).”

“A low risk sensitivity of capital requirements undermines the ability of banks to withstand adverse shocks…”

- First, we show the capital buffers that banks typically hold above regulatory requirements partly result from capital arbitrage [A practice whereby firms capitalize on loopholes in regulatory systems. Arbitrage opportunities may be accomplished by a variety of tactics, including restructuring transactions, financial engineering and geographic relocation.]. This means that banks with higher capital buffers report lower amounts of risk-weighted assets per unit of assets for a given level of portfolio risk.

- Second, we show that capital arbitrage diminishes banks’ ability to withstand adverse shocks. We show that banks that increased their capital buffers markedly during 2008 and 2009 and did so relying at least in part on government support displayed a particularly low risk sensitivity of their capital requirements between 2000 and 2007.

Implication for current capital regulation reform

“The Basel III revisions are designed to increase both the quantity and quality of minimum capital holdings by further enhancing the risk sensitivity of capital requirements. As regards increases in risk-weighted assets relative to Basel II, the Basel Committee reports that ‘a 1.23 factor is a rough approximation based on the average increase in [risk-weighted assets] associated with the enhancements to risk coverage in Basel 3 relative to Basel 2’. However, as long as the regulatory concept of risk exposure underlying the computation of risk-weighted assets remains only weakly related to risk, the proposed increases in capital requirements are unlikely to align capital holdings with the effective riskiness of bank asset portfolios. The risk sensitivity of capital requirements we report is of such a low magnitude that we question whether Basel III will improve the relationship between capital requirements and risk in an economically meaningful way. The projected increase in risk-weighted assets under Basel III suggests that – even under a minimum capital ratio of 13% – banks in our sample will only be required to hold, on average, 1.94% of additional capital per unit of assets. Such an increase is unlikely to make minimum capital requirements more reflective of bank portfolio risk in an economically meaningful way.”