The IMF projects that 2013 will see a big reduction in the developed world’s fiscal deficit by roughly 1.5%-points to 4.5% of GDP. By now the majority of highly-indebt countries seems to have achieved about two-thirds of the required post-crisis fiscal consolidation. The advanced countries’ public debt stock remains elevated at 109% of GDP, however, leaving the world vulnerable to higher interest rates and sovereign solvency risks.

International Monetary Fund, “Fiscal Monitor – Taxing Times “, October 2013

http://www.imf.org/external/pubs/ft/fm/2013/02/fmindex.htm

The below are excerpts from the report. Cursive texts, emphasis and brackets have been added.

The declining global fiscal deficit

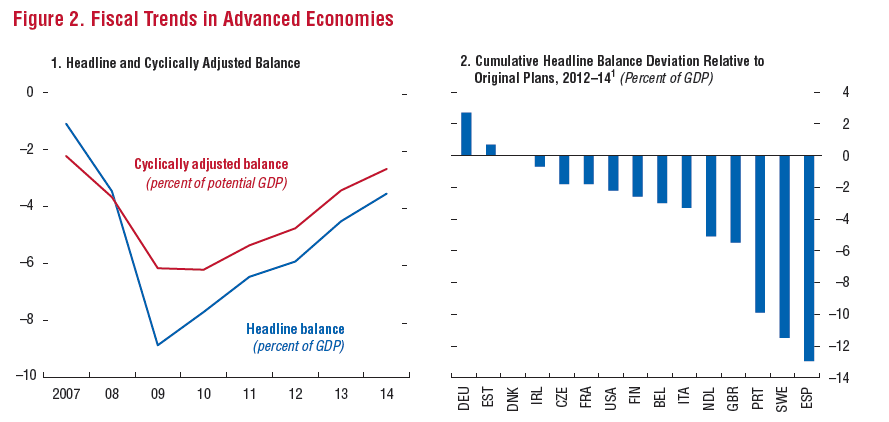

“The average fiscal deficit of advanced economies is set to narrow by 1.5% of GDP in 2013 in both headline and cyclically adjusted terms, the fastest pace since consolidation efforts started in 2011…[The overall deficit is projected to decline to 4.5% of GDP in 2013, from 5.9% in 2012, and a trough of 8.9% in 2009. The cyclically-adjusted deficit is estimated to reach 3.4% of GDP in 2013, after 4.8% in 2012, and 6.2% in 2009].”

“In the face of worsening cyclical conditions, many emerging market economies are postponing consolidation. The headline overall balance for this group is expected to continue deteriorating in 2013 and broadly stabilize in 2014, albeit in many cases at still relatively contained levels…[The headline deficit of EM countries is projected to increase to 2.7% of GDP in 2013, from 2.1% in 2012, and 4.6% in 2009. The cyclically-adjusted deficit is estimated to rise to 2.3% of GDP, after 2.1% in 2012, and 3.5% back in 2009].”

“Although fiscal adjustment has picked up in 2013, headline overall balances remain in most countries weaker than projected when the fiscal correction phase started in 2011, reflecting slower-than-expected growth. In only a few countries (importantly, Germany and the United States) have fiscal developments proved generally close to plans drawn back in 2011, likely because original growth projections were close to actual outcomes…In most countries… lower growth led to a relaxation of headline deficit targets. These include euro area countries, such as those for which the European Council recently (in June 2013) sanctioned extending the deadline to attain the 3% deficit target.”

“Although 2014 budgets are in most cases still to be fleshed out, fiscal tightening is expected to moderate significantly next year as a large part of the consolidation has already taken place or is close to completion. On average, close to two-thirds of the adjustment required to reach medium-term targets has been achieved in the 10 most highly indebted countries, with the notable exception of Japan.”

“Notwithstanding progress on fiscal consolidation, underlying fiscal vulnerabilities remain elevated in many advanced economies, reflecting persistently high debt, increasing uncertainty about the growth and interest rate environment, and failure to address long-term spending pressures… Age-related spending remains a key source of medium-term vulnerability, with projected growth of more than 4 percent of GDP in advanced economies and 3¼ percent of GDP in emerging market economies through 2030. The growth of public health spending has slowed across the board in advanced economies over the past three years, but econometric analysis suggests this is due more to deteriorating macroeconomic and fiscal conditions than to structural improvements.”

Some important country developments

“In the United States, the cyclically adjusted balance is projected to improve by 2.25% of potential GDP in 2013 [to 3.9% of GDP from 6.3% in 2012, and 8% in 2010] and another 0.75% in 2014, cumulatively some 1.5% percent of GDP more than previously projected, reflecting the extension of automatic spending cuts (the sequester) into 2014, as well as unexpected revenue strength. In addition to the untimely drag on short-term activity, the indiscriminate expenditure cuts could also lower medium-term growth prospects by falling too heavily on productive public outlays. [The government debt stock in the U.S. is expected to climb to 106% of GDP in 2013, from 73% in 2008.]”

[The euro area’s cyclically adjusted deficit is projected to just 1.6% of GDP in 2013, from 2.7% in 2012, and a trough of 5% in 2009. Greece is projected to reach a cyclically-adjusted surplus of 0.6% of GDP. Germany’s budget is seen in balance. High deficits are expected for Ireland at 5.1% and Spain at 4.6% of GDP…The gross debt stock in the euro area is expected to reach 96% of GDP this year, compared to 70% in 2008.]

“In the United Kingdom, the cyclically adjusted balance is projected to improve by close to 2% of GDP in 2013 [to 4% of GDP in 2013, from 5.8% in 2012, and 10.3% in 2009] —of which 1 percent is accounted for by the transfers of profits from the Bank of England’s asset purchases to the Treasury, and the rest largely by discretionary measures. Consolidation is expected to continue in 2014, with planned measures of about 1 percent of GDP. [The general government’s gross debt stock is projected to reach 92% in 2013, from 52% in 2008.]”

“Japan continues to postpone consolidation, with the cyclically adjusted primary deficit projected to remain about 8.5% percent of GDP in 2013. [The cyclically adjusted total deficit is projected to remain stable at 9.2% of GDP]. In 2014 and 2015, significant tightening is expected, with a two-step increase in the consumption tax rate. The recently announced decision to go forward with the first stage of the consumption tax increase to 8% in April 2014 is a welcome step. [Gross government is projected to rise to 243% of GDP in 2013 from 192% in 2008.]”