A Nomura research report suggests that China’s local government financing vehicles now pose a major risk for the economy. Their debt stock has surged close to 40% of GDP over the past three years. Profitability is poor, liquidity risks are high, and solvency hinges on government support.

China’s heavy LGFV debt burden

(The report is proprietary research of Nomura International. For access please contact the institution)

The below are excerpts from the report. Cursive text and emphasis has been added.

What are local government financing vehicles?

“Local government financing vehicles, or LGFVs, are entities set up by local governments to raise funds primarily for public infrastructure projects. Most local governments are forbidden by the central government to run a deficit or borrow… While owned by the local government, [LGFVs] can raise funds through the more traditional methods of taking bank loans, issuing bonds, and via equity market initial public offerings, as well as via shadow banking activities such as trust loans.”

How large is LGFV debt?

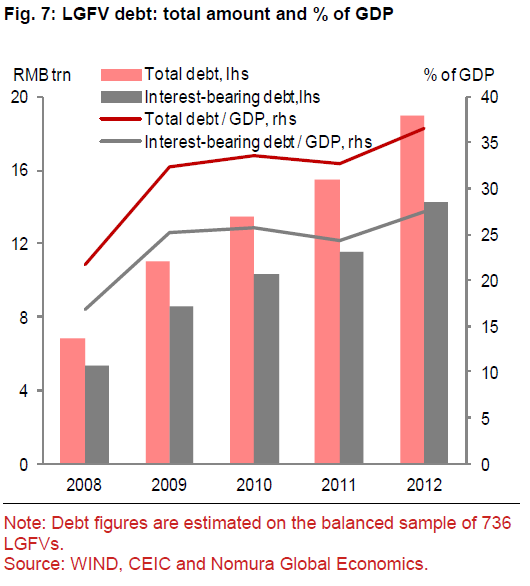

“Local government financing vehicles have accumulated massive debts since 2009 and now pose a major risk to the economy…We use a unique, bottom-up approach to assess the financial risks of 869 LGFVs, which accounted for 72% of total LGFV debt in 2012″

“We estimate total LGFV debt at the end of 2012 was RMB19.0trn (37% of GDP), which included RMB14.3trn of interest-bearing debt. In the period 2010-12, LGFV debt rose by 39%, which implies total government debt of RMB31.7trn, or 61% of GDP at end-2012…LGFVs played a pivotal role in helping to finance infrastructure investment – one of the pillars of China’s recent economic growth – and official data now show LGFVs account for 14.7% of outstanding bank loans…Our analysis may underestimate the true size and risks in LGFV debt. Our study is based on LGFVs that have issued bonds – and these are likely to be in better financial condition than those that cannot issue bonds.”

“While LGFV debt-to-GDP may appear manageable at the national level, the debt-to-fiscal revenue ratio suggests that LGFV debt remains a heavy burden for local governments. Our estimate of LGFV debt is that it will reach 311% of local government budgetary revenue in 2012. We also estimate that, if the central government’s fiscal transfers to local governments are added, the ratio of LGFV debt to local government fiscal revenue would be lower, at 179%.”

Why is LGFV debt an increasing systemic concern?

“We find LGFVs in our sample face a number of serious financial risks:

- Liquidity conditions are tight and worsening. Demand for funding continues to grow, yet profitability and operating cash flows fell sharply in 2012. 35% of LGFVs experienced net operating cash outflows and hence have to rely on new borrowing to finance existing investment activities…The reported profitability of LGFVs is low and falling quickly, which means their capacity to repay debt is questionable. The median ROE [return on equity] fell from 4.1% in 2009 to 3.0% in 2012, far below the 7.5% median ratio for A-share listed nonfinancial companies

- Solvency for many LGFVs depends on asset injections from local governments and debt restructuring… The practice of “capital injections” [mostly land transfers] is pervasive in the LGFV sector, as they need to maintain a reasonable debt-to-asset ratio in order to borrow from banks and issue new debt…Many assets injected are illiquid and hence would be of little help in a liquidity crisis… Harbin Urban Construction Company illustrates this well. In 2012 it became one of the largest LGFVs in the country after the local government injected timber resources worth RMB72.6bn into it, raising its total assets by 35% – but we doubt its resources could be liquidated easily to help repay debt if necessary, particularly in a systemic financial crisis… Another method of “boosting” a balance sheet is to remove the liabilities. Yunnan Highway Company – which reportedly defaulted on its bank loans in 2011 – saw a remarkable turnaround in its financial conditions… due to the quiet removal of RMB20bn of debt (25% of its total debt) from its balance sheet. To the best of our knowledge there has been no disclosure of where this debt went.

- LGFV debt is sensitive to an interest rate shock. Our stress tests find that if interest rates rise by 100bp, an additional 10.4% of LGFV debt would become non-sustainable.”

“A majority of LGFVs rely on fiscal subsidies and aggressive accounting practices to service their debt. Adjusting for these, we estimate that over half would have been at risk of default in 2012. In a liquidity crisis, we estimate that 70% would have defaulted…Dangerously, LGFVs are relying increasingly on new debt to finance long-term investments.”

“Systemic risks are rising quickly. With government revenues under pressure, interest rates rising and local government land revenues facing uncertainty due to an unsustainable property boom, the number of LGFV credit rating downgrades has risen recently. Moreover, the continued practice of using land and property as collateral is questionable. These factors will likely exacerbate LGFV debt conditions in 2014.”