The view that high public debt is bad for growth, popularized by Reinhart and Rogoff, has failed to find much empirical support in academic research. A paper by Lof and Malinen presents evidence that over the past 55 years lower growth has typically preceded higher debt but higher debt has not usually preceded lower growth.

“Determinants of the growth and sovereign debt correlation”, Matthijs Lof and Tuomas Malinen, post on VOX website, 25 May 2014

http://www.voxeu.org/article/growth-and-sovereign-debt-correlation

“Does sovereign debt weaken economic growth? A Panel VAR analysis”, Matthijs Lof and Tuomas Malinen , Economics Letters 122/3, 403-407

The below are excerpts from the post. Cursive lines and emphasis have been added.

Questioning the debt-growth causality

“Reinhart and Rogoff…argue that high debt may lead to higher taxes and/or lower government expenditure, which is harmful for economic growth… While the research by Reinhart and Rogoff had a substantial influence in policy circles, their [empirical] results are controversial. Last year, researchers from the University of Massachusets Amherst revealed a number of computational errors.”

“Even if a negative correlation between debt and growth seems undisputed, this does not imply that debt is harmful for growth, since correlation does not always imply causation.”

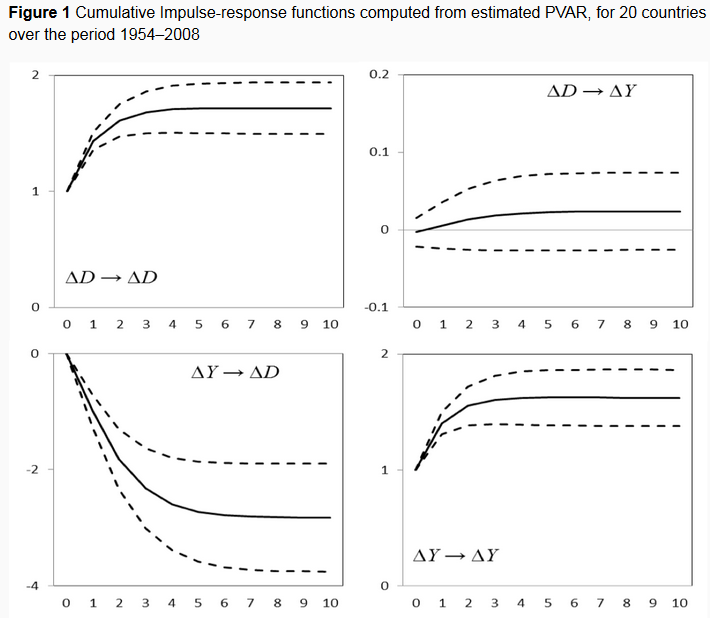

“We estimate a VAR [vector autoregression] for sovereign debt and GDP growth on panel data for 20 OECD countries over a period of 55 years, which we obtain from the dataset of Reinhart and Rogoff (2009)… a VAR treats both debt and GDP as endogenous. Both are allowed to have an impact on each other, and these impacts can be separated… we can visualise the long-run impact on both variables after a shock hits one of the variables.”

N.B. Vector autoregression is an econometric model for the evolution of two or more variables overtime. The model relates each variable to its own past value and the past value of the other variables (and a random shock). The relations are simply linear. Once their coefficients are estimated one can construct impulse-response functions that depicts the impact of a normal “shock” (unexpected change) in one variable on all others. These functions tell a story of past empirical regularity and do not necessarily imply causality.

“[The figure below] shows the cumulative impulse response functions from the estimated panel VAR. The solid line shows the estimated cumulative impact over a period of 10 years on debt (left column) and GDP (right column), after a positive shock to either debt (top row) or GDP (bottom row). The dashed lines show the 95% confidence interval.

- A positive shock to debt (i.e. an increase in debt) seems to have no negative impact on GDP. The point estimate of the impact is in fact even positive, but the confidence interval is so wide that the effect is not significant.

- On the other hand, the bottom-left panel shows that a positive shock to GDP does have a significant negative impact on debt, which explains the negative correlation between debt and GDP.”

“Finally, we investigate the idea of a threshold effect, or ‘tipping point’, in the relation between debt and growth. Reinhart and Rogoff argue that the negative correlation increases after the level of debt exceeds 90% of GDP…To analyse this issue in the VAR framework, we divide the sample into high-debt and low-debt countries…The results are clear: The relation between debt and GDP is remarkably stable across high-debt and low-debt countries…There is no evidence for a negative effect of debt on growth, not even for elevated levels of debt.”