Marco Dion, Viquar Shaikh and colleagues at J.P. Morgan Cazenove illustrate how the information value of equity dividend yield can be enhanced. Their measure of “shareholder yield” integrates dividends with other forms of cash returns, i.e. share buybacks and debt redemption. They present evidence that for U.S. and European stocks the enhanced measures creates alpha for systematic trading styles.

J.P. Morgan Cazenove, Quant Forensics: Volume 5

“When studying dividend and dividend based strategies, we find that not all companies should be considered equal as not all companies pay dividends and not all managements consider dividend as an essential method of rewarding investors…many large companies spend a substantial amount of money in share buy-backs and/or debt repayment.”

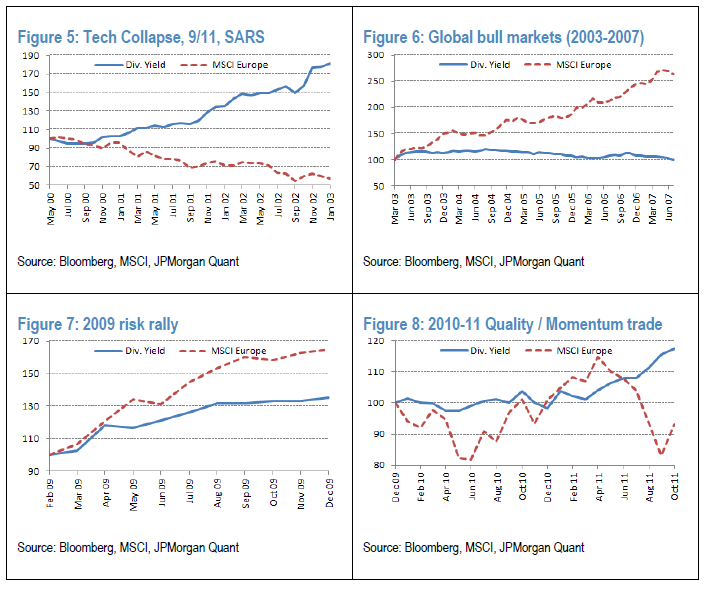

“Dividend Yields and companies’ usage of their excess cash have seen a greater scrutiny since the sub-prime crisis…Dividend Yield appears attractive to risk-averse investors as it enjoys better performance during volatile and unstable periods.”

“Academics and practitioners alike have over the years questioned the wisdom of using only dividends as a means of returning cash to the shareholders when there could be other (and arguably better) ways of increasing the shareholder value.”

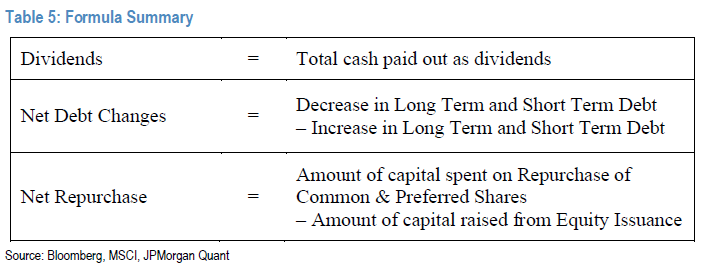

“We…create a single Factor (“Shareholder Yield”) that combines all these three components.”

N.B.: “The biggest task we faced when producing this analysis was sourcing the data. While cash-flow statements data, if sourced from certain third party providers, can potentially go back until the 1970s, that coverage is mostly restricted to names from the US… financial statement data on Bloomberg (or Reuters Global Fundamental database etc), goes back until only the late 80s/early 90s for some names, though the coverage only starts getting meaningful towards the late 90s/early 2000s.”