Morgan Stanley’s Viktor Hjort, Nishant Sood, and Gaurav Singhal show that financial leverage of China’s corporates has reached record highs, particularly for state-owned enterprises (SOEs). Increased debt financing reflects easy credit conditions and has partly served to cover funding gaps. In case of an economic downturn, consequences for credit quality would probably be more severe now than back in 2009.

Leveraged China

Morgan Stanely Asia Credit Strategy, May 3, 2013

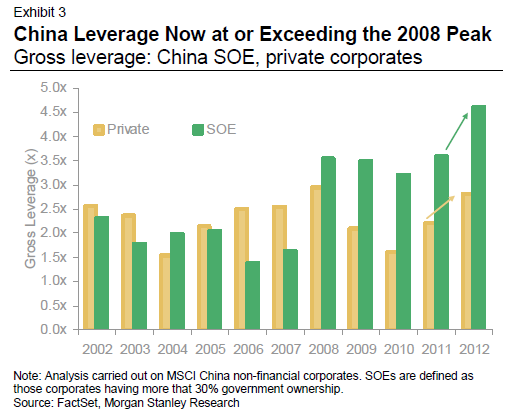

“A combination of rapid credit growth and a sluggish economic environment in the past year has pushed corporate leverage to record highs in China…The broadest quality measure of corporate leverage (MSCI China’s non-financial corporate universe) reached an all-time high of 3.1x (gross debt/EBITDA), driven by SOEs (4.6x), more than a turn higher than during the 2008 downturn, and to a lesser degree private sector corporates (2.8x) still short of the 2008 levels.”

“The credit quality of Corporate China is deteriorating and is now at a point where we think it’s going to become a headwind for further outperformance…The fastest credit quality deterioration is in the parts that dominate credit markets: SOEs, industrials and to some extent property…All three are key components of the traded bond universe, together accounting for more than 20% of the total risk in Asia credit and over 85% of the risk contribution from China: SOE (IG) leverage increased by a turn, private sector industrial leverage (HY) by 0.8x and property (HY) by 0.7x.”

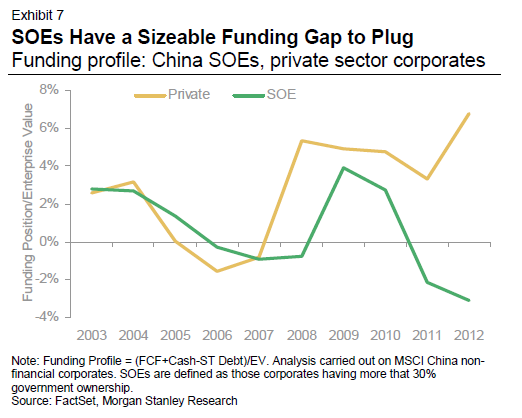

“The bulk of leverage sits with SOEs who, on average, also generate less return on assets…SOEs’ debt raising today is mainly about plugging a fairly persistent funding gap. Growth is sluggish and the capex trend is moderating but the funding position (defined as starting cash less short-term debt plus free cash flows over the year) for SOEs began to deteriorate in 2010, turned negative in 2011 and continued to worsen in 2012.”

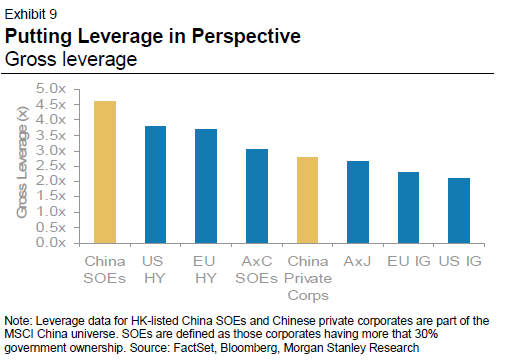

“Leverage for the median listed China SOE is 4.5x, about half-to-one turn higher than US and European sub-investment grade companies are today and higher than other regional SOEs. 4.5x is also roughly where US sub-investment grade corporates are in recessions and typically associated with 10-12% default rates.”