A Bank of Italy paper illustrates and explains the rise in European banks’ sovereign debt holding since the great financial crisis. It also reiterates structural causes for bank-sovereign feedback loops. One would conclude that this nexus remains an important factor for market dynamics and monetary policy.

“The negative feedback loop between banks and sovereigns”, Paolo Angelini, Giuseppe Grande and Fabio Panetta, Banca d’Italia Occasional Paper 213, January 2014

http://www.bancaditalia.it/pubblicazioni/econo/quest_ecofin_2/qef213/QEF_213.pdf

The below are excerpts from the paper. Emphasis and cursive text has been added.

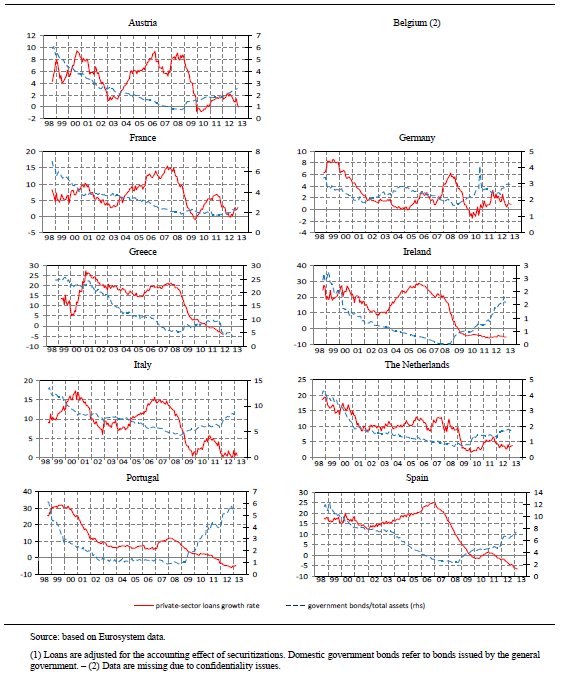

“Banks in virtually all European countries had been reducing their exposures to their domestic sovereign (indeed, to all euro-area sovereigns) for several years, but in the Fall of 2008, after the Lehman default, they resumed purchases.”

“What were the mechanisms whereby the crisis triggered a resurgence of the home bias from the end of 2008 on? … Evidence suggests…that the recent expansion of banks’ government securities portfolios is a consequence, not a cause, of the crisis…

- Moral suasion: high-risk sovereign issuers may exert ‘moral suasion’ on their domestic banks, asking them to support demand for sovereign debt.

- Gambling for resurrection: undercapitalized banks may have gambled for resurrection ’by engaging in carry trades – getting cheap liquidity from the ECB and investing it in high-yielding bonds, which absorbed little if any capital…[In Italy] consistent with ‘gambling for resurrection’…large purchases of government paper were also observed among other financial intermediaries.

- Re-nationalization: banks wishing to hedge redenomination risk gradually moved to match their assets and liabilities at the national level, replacing foreign assets with domestic ones…

- Precautionary motive: in the second half of 2011, with the escalation of the sovereign debt crisis, wholesale markets had all but frozen. Euro-area banks, especially those of countries under stress, had become unable to roll over their wholesale debt. Therefore, they took ample advantage of the 3-year LTROs [long-term repo operations] and invested the funds in government securities, which could be easily liquidated to reimburse maturing wholesale bonds, if conditions for new issuances continued to be prohibitive…

- Yield motive: from 2011 on the risk-adjusted differentials between returns on investments in securities and returns on loans to resident customers in Italy widened considerably. Therefore, banks chose the most profitable investment. This explanation is different from the gambling for resurrection/carry trade hypothesis.”

How sovereign risk is transmitted to banks

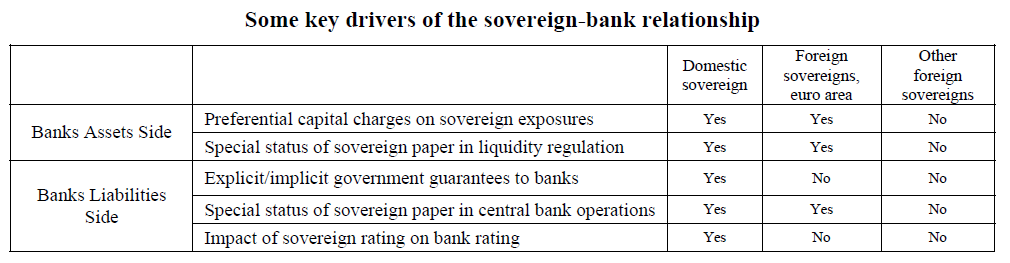

“Deterioration… in a government’s creditworthiness…may cause…losses…on banks’ portfolios of sovereign securities and…their loans to the government…Sovereign exposures… are often substantial… [while] direct exposure to foreign sovereign debt is ordinarily limited…Current regulations…give claims on the government preferential treatment over those on private borrowers…partly reflecting the Basel II framework, de facto zero risk weights are granted to most of the debt issued by EU sovereigns.”

“Sovereign strains [affect] bank funding… also in terms of liquidity…. Since government bonds are typically used as collateral, e.g. in repos, a fall in their price can trigger margin calls or larger haircuts, thus reducing the liquidity that can be obtained via a given nominal amount of sovereign paper. Related to this, in most countries government paper is typically given preferential treatment as collateral in central bank operations. It is also assigned an important role in the Basel III liquidity framework via the so-called liquidity coverage ratio. ”

“Several governments introduced explicit guarantee schemes on bank bonds after the collapse of Lehman Brothers in October 2008. There is evidence that these guarantees helped reduce risk premia on banks’ liabilities, and that their effect was proportional to the creditworthiness of the sovereign…Implicit guarantees are harder to measure, but there is evidence that they may be among the reasons why on average large banks borrow at a discount.”

“Sovereign downgrades often lead to downgrades of domestic banks, not least because the sovereign rating normally represents a ceiling for the ratings assigned to private borrowers. Downgrades reduce the value of banks’ liabilities; loss of investment grade status can make them ineligible as collateral in funding operations, or as investments suitable for certain categories of investors, such as pension funds and insurance companies.”

How bank risk is transmitted to sovereigns

“A financial crisis may require the government to support banks and other financial institutions… In late 2008-early 2009 the magnitude of this support was unprecedented…In some cases (Ireland, Iceland, and more recently Cyprus) the size of the banking problem was as large as to jeopardize the sovereign.”

“A credit squeeze will weaken the economy, leading to a decline in borrowers’ creditworthiness and to further tensions in the sovereign’s situation, due to falling fiscal revenues and the need for further fiscal tightening.”

Empirical findings on the bank-sovereign nexus

“From the analysis of credit risk premia (gauged by CDS contracts and banks’ exposure to the domestic sovereign), three facts stand out.”

- “First of all, within the euro area the sovereign-bank link, as indicated by the correlation between the CDS premia for the sovereign and banks, is no stronger than the link between sovereigns and domestic non-financial corporations, both before and after June 2011…

- Second, there is no clear connection between the proportion of banks’ assets consisting in domestic government securities and the sovereign-bank correlation…

- Third, in all the countries of the area the proportion declined steadily from the mid-1990s through to the end of 2008, and turned up again in the following years. In Italy, the same pattern is found for insurance companies and pension funds.”