The European Financial Stability Facility (EFSF) and its permanent replacement, the European Stabilization Mechanism (ESM) haven proved less effective than the ECB in quelling crisis dynamics. However, the funds are large in size and will play major role in the euro area’s institutional response to crisis pressue.

Source: Conversations with market economists, various broker research, and http://www.esm.europa.eu/

The EFSF was created by the euro area Member States on 9 May 2010 with a mandate to raise funds in capital markets for the purpose of preserving financial stability of Europe’s monetary union through temporary financial assistance to euro area Member States.

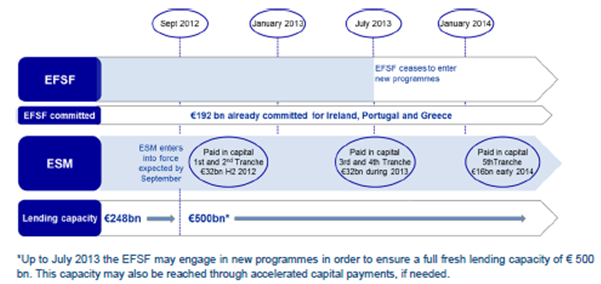

As to its financial capacity in June 2011 the head of Government and State agreed to broaden the EFSFs scope of activity and increase its guarantee commitments to EUR780 bn from EUR440 bn. This corresponds to a lending capacity of EUR440 billion (about 5% of euro area GDP). The European Financial Stability Facility was designed as a temporary addition to a wider safety net. The means of the EFSF wereviewed in conjunction with lending capacity of up to EUR60 bn from the European Financial Stabilisation Mechanism (EFSM, funds raised by the European Commission and guaranteed by the EU budget) and up to EUR200 bn from the International Monetary Fund.

In order to fulfill its mission, the EFSF is authorised to: (1) issue bonds or other debt instruments on the market, (2) intervene in the debt primary and secondary markets, and (3) finance recapitalisations of financial institutions through loans to governments. All financial assistance to Member States is linked to appropriate conditionality.

According to the Treaty on the ESM: “The liability of each ESM Member shall be limited, in all circumstances, to its portion of the authorised capital stock at its issue price. No ESM Member shall be liable, by reason of its membership, for obligations of the ESM. The obligations of ESM Members to contribute to the authorised capital stock in accordance with this Treaty are not affected if any such ESM Member becomes eligible for, or is receiving, financial assistance from the ESM”

The ESM’s effective lending capacity will be EUR500 billion. However, following the Eurogroup meeting held on 30 March, it was decided that the EFSF would remain active until July 2013. The combined lending capacity of EFSF/ESM is illustrated by the diagram below. Overall lending will not exceed EUR500 billion.

In the opinion of the European Central Bank the ESM funds cannot be leveraged with the help of the eurosustem: “With respect to the role of the ECB and the Eurosystem, while the ECB may act as fiscal agent for the ESM…Article 123 Treaty on the Functioning of the European Union (TFEU) would not allow the ESM to become a counterparty of the Eurosystem under Article 18 of the Statute of the ESCB. ..The ECB recalls that the monetary financing prohibition in Article 123 TFEU is one of the basic pillars of the legal architecture of EMU.”

(Source: Opinion of the ECB of 17 March 2011 on a draft European Council Decision amending Article 136 of the Treaty on the Functioning of the European Union (TFEU) with regard to a stability mechanism for Member States whose currency is the euro.)