Variance swaps are over-the-counter derivatives that exchange payments related to future realized price variance against fixed rates. Variance swaps help estimating term structures for variance risk premia, i.e. market premia for hedging against volatility risk based in the difference between market-priced variance and predicted variance. The swap rates conceptually produce more accurate estimates of variance risk premia than implied volatilities from the option markets. An empirical analysis suggests that swap-based variance risk premia are positive and increasing in maturity. A drop in equity prices or rise in credit spreads pushes variance risk premia higher. The effect is strongest for short maturities up to 6 months, but more persistent for long maturities.

The post ties in with SRSV’s summary lecture on implicit subsidies, particularly the part on sources of implicit subsides and elevated risk premia paid by financial institutions.

The below are quotes from the paper. Emphasis and cursive text have been added.

What are variance swaps?

“Over the last two decades, the demand for volatility derivative products has grown exponentially, driven in part by the need to hedge volatility risk in portfolio management and derivative trading…Among volatility derivatives, variance swap contracts can be thought of as the basic building block. These are in principle simple contracts: the fixed leg agrees at inception that it will pay a fixed amount at maturity, the VS rate, in exchange for receiving a floating amount based on the realized variance of the underlying asset, usually measured as the sum of the squared daily log-returns, from inception to maturity. The payoff of a variance swap therefore depends on the actual trajectory of the underlying asset through its realized variance.”

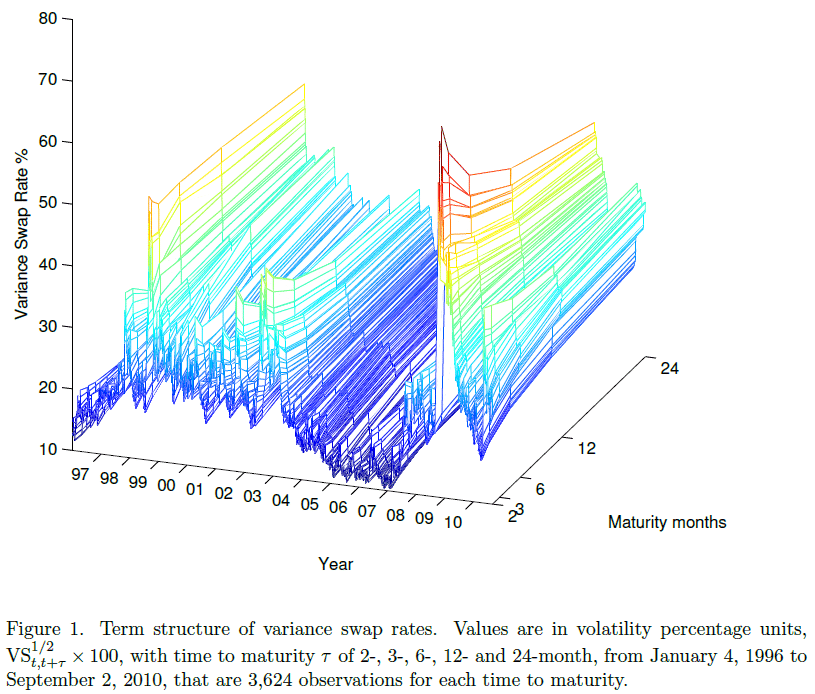

“The variance swap market…is a relatively unexplored market compared to option markets and one that is becoming increasingly important… variance swap contracts are typically traded for various maturities ranging from two months to two years.”

“Interestingly, variance swap rates are on average higher, more volatile, skewed, and leptokurtic than VIX-type [implied volatility] indices for each maturity. Moreover, the difference between variance swap rates and implied volatilities increases with the time to maturity. Such differences are mostly positive, statistically significant, larger during market turmoil but sizeable also in quiet times… the gap between variance swap rates and implied volatilities is consistent with the presence of a significant price jump component embedded in variance swap rates.”

What is the integrated variance risk premium?

“Focusing on the variance swap term structure [as opposed to implied volatility term structure] allows us to accurately estimate the term structure of variance risk premia… The variance swap term structure provides directly the market price, or risk neutral expectation, of future realized variances. By contrast, option implied volatilities reflect future realized variances but also other factors such as interest rates or dividends.”

“We define the integrated variance risk premium as the difference between the objective and risk neutral expectations of future realized variance over a fixed time horizon. In other words, the integrated variance risk premium is the ex-ante expected profit to the long side of a variance swap contract. “

What can we learn from variance risk premia and their term structure?

“This paper investigates the term structure of variance swap rates, which arises by varying the maturity of the variance swap contract… from two months to two years. We then infer from these data the term structure of…variance risk premia. Studying the term structure of variance swap rates and risk premia provides insights on how investors’ perceive risk and which economic variables influence this perception.”

“The model-free analysis above indicates that variance swap rates embed a price jump component.”

“To further the analysis of the variance swap term structure, we therefore employ a parametric stochastic volatility model. The model is consistent with the salient empirical features of variance swap rates that we document in the model-free analysis, and takes the form of a two-factor stochastic volatility model with price jumps and variance jumps.”

“Our model-based analysis shows that the integrated variance risk premium is negative and usually exhibits a downward sloping term structure.

- A negative risk premium indicates that the variance swap holder is willing to pay a large premium, the variance swap rate, to buy protection against volatility risk, which in turn induces an expected negative variance swap payoff… Thus, shorting variance swap contracts is profitable on average. However, realized variances are also more volatile, positively skewed and leptokurtic than variance swap rates, which highlights the riskiness of shorting variance swap contracts. The large variability and in particular the positive skewness of ex-post realized variances can induce large losses to the short side of the contract.

- The downward sloping term structure means that the longer the maturity of the variance swap the more negative the expected variance swap payoff… Thus, shorting long-term variance swaps is on average more profitable than shorting short-term variance swaps…Moreover, after a volatility spike, investors’ willingness to ensure against future volatility risk increases with the time to maturity. This effect is stronger over short maturities, such as two months, but more persistent over long maturities, such as two years.”

“The contribution of price jumps is modest in quiet times, but important during market drops, and mostly impacts the short-end of the integrated variance risk premium term structure. Thus, short-term variance risk premia substantially reflect investors’ fear of a market drop. This finding indicates that theoretical asset pricing models seeking to explain asset returns and their volatility in the short run should feature price jumps [and] investors’ aversion to jump risk.”

“Through regression analysis, we show that the term structure of integrated variance risk premium reacts to variables proxying for equity, option, corporate and Treasury bond market conditions.

- Not surprisingly, a drop in the S&P500 index induces a more negative integrated variance risk premium, but this effect quickly dies out in the term structure of the integrated variance risk premium, becoming statistically insignificant beyond a 6-month time to maturity. In other words, daily changes of the S&P500 index strongly impact investors’ perception of volatility risk, but only over short maturities.

- Similarly, an increase of corporate credit riskiness increases the integrated variance risk premium in absolute value but only up to a 6-month time to maturity. The variance swap market participants seem to view changes in credit riskiness as a transient phenomenon in terms of its impact on volatility risk.”