Modern dealer bank financing relies largely on collateralized transactions. In order to achieve collateral efficiency institutions engage in rehypothecation, for example through matched-book transactions, internalizing trading activities, and re-pledging of margin collateral. A New York Fed article suggests that this funding structure faces risks from rollover, credit rating downgrades, and reputational considerations.

“Matching Collateral Supply and Financing Demands in Dealer Banks”

Adam Kirk, James McAndrews, Parinitha Sastry, and Phillip Weed

http://www.ny.frb.org/research/epr/2014/1403kirk.pdf

The below are excerpts from the article. Emphasis and cursive text has been added.

How dealer bank financing works – in a nutshell

“Dealer banks are active in the intermediation of many markets, either in their role as dealers or in their role as prime brokers where they provide financing to investors… Services typically provided by dealers include buying and selling the same security simultaneously, extending credit and lending securities in connection with transactions in securities, and offering account services associated with both cash and securities.”

“Dealer banks rely on…unique sources of funding. In most cases, dealer banks’ lending is collateralized by securities or cash. As in a standard bank, funding for a loan made by the bank may come from…equity or from external sources…Unlike a standard bank, however, dealer banks can employ internal sources to fund a customer loan, either by taking a trading position that offsets that of the customer receiving the loan or by utilizing an offsetting position taken by another customer.”

“For example, the bank may make a ‘margin loan’ to one customer, lending cash to finance the customer’s security purchase with the customer offering the purchased security as collateral for the bank loan. Another customer may request to borrow the same security to establish a short position, offering cash to the bank as collateral for the loan. The two customers’ pledges of collateral provide the bank with the resources to fulfill both customers’ demands for borrowing.”

“We review three [efficient mechanisms of collateral reuse]: matched-book financing, internalization of collateral financing, and pledging of collateral received in over-the-counter (OTC) derivatives trading…

- In a typical matched-book transaction, a client provides a security as collateral in exchange for cash and grants the dealer the right to repledge this collateral. The dealer repledges this security to another client to source the cash. As a result, the dealer’s balance sheet does not reflect any security owned…

- Dealers achieve yet another source of collateralized financing efficiency by ‘internalizing’ their trading activities… by using offsetting trading positions between two clients or between clients and the dealer bank to ‘finance’ each other… opportunities to “internalize” can arise via the provision of funds by the dealer bank collateralized by client securities. Those securities are then reused and delivered into another transaction as a means of financing the client position…

- Collateral received or posted in relation to secured derivatives transactions… generate[s] or use[s] cash through receiving or posting initial margin and variation margin, which serve to offset the risks associated with current and potential future exposure, respectively… Unlike other secured transactions…the derivatives transactions as defined here do not entail the exchange of cash for securities, but rather the posting or receipt of collateral to secure an economic claim.”

The netting issue

“Under both U.S. and international accounting standards, the exposure of a dealer bank to a customer that has offsetting collateralized positions with the dealer bank can be reported as the net economic claim…Suppose…Customer A borrows cash and provides a security as collateral to the dealer bank; suppose furthermore that Customer B borrows the security and provides cash collateral to the dealer bank. The dealer bank uses the collateral provided by one customer to satisfy the borrowing demands of the other. Now suppose that, later, Customer B borrows cash and proffers a different security to the dealer bank as collateral, and Customer A borrows that security and supplies cash to the dealer bank as collateral. Then…the dealer may be eligible to be net on the balance sheet of the dealer, the dealer may be able to report assets and liabilities equal to $0.”

How this leads to vulnerability

“The stock of net collateral received by a dealer bank is exposed to certain vulnerabilities that call to question its overall durability as a means of financing, even under circumstances where the offsetting transactions are matched in terms of market risk and level of collateralization.

- First… transactions are subject to…rollover risk…. At the maturity of a swap transaction, unless the position is rolled over, the collateral received would need to be returned to the original client. If a dealer offsets a position with one of shorter duration, or if a dealer obtains some amount of net collateral received on transactions of matched duration, at maturity it faces a financing gap in the amount of the margin posted to the offsetting transaction…

- Second, from the contractual perspective, transactions are often embedded with certain credit rating downgrade triggers requiring the posting of additional collateral or imposing more constraining restrictions on rights of rehypothecation…

- Finally, dealer banks may be beholden to reputational considerations in periods of stress. While they may have contractual rights over the use of client collateral, they may nevertheless honor client requests to segregate collateral or close out trades pre-emptively in the spirit of preserving their franchise…[This] undermines the durability of net collateral received in relation to derivatives as a source of dealer financing.”

“This vulnerability of dealer banks, though similar to that faced by standard banks when depositors withdraw, differs in that it occurs instead when borrowers repay their loans… we find that the experience of the financial crisis was especially troubling for dealer banks. The collateral they had received from customers disappeared when customers exited positions that the dealer bank had financed. Because dealer banks had heavily utilized the customer-provided collateral, they were forced to source collateral and cash externally to manage and meet their obligations at the same time that markets were most disturbed. Notably, the dealer banks’ brokerage receivables were most affected by the crisis, plummeting significantly more than the firms’ other sources of collateral and much more than the balance-sheet assets of the firms. This likely is the result of the significant moves in markets, including the equity markets, which at the height of the crisis led customers to exit leveraged bets,”

“Internalization [in particular] is vulnerable to a unique set of risks, as it relies on the market positioning of customers. As conditions in markets change, due to a significant price move, for example, either one side or the other might rapidly exit its financing position from the dealer, forcing the dealer to quickly replace securities or cash from external markets.”

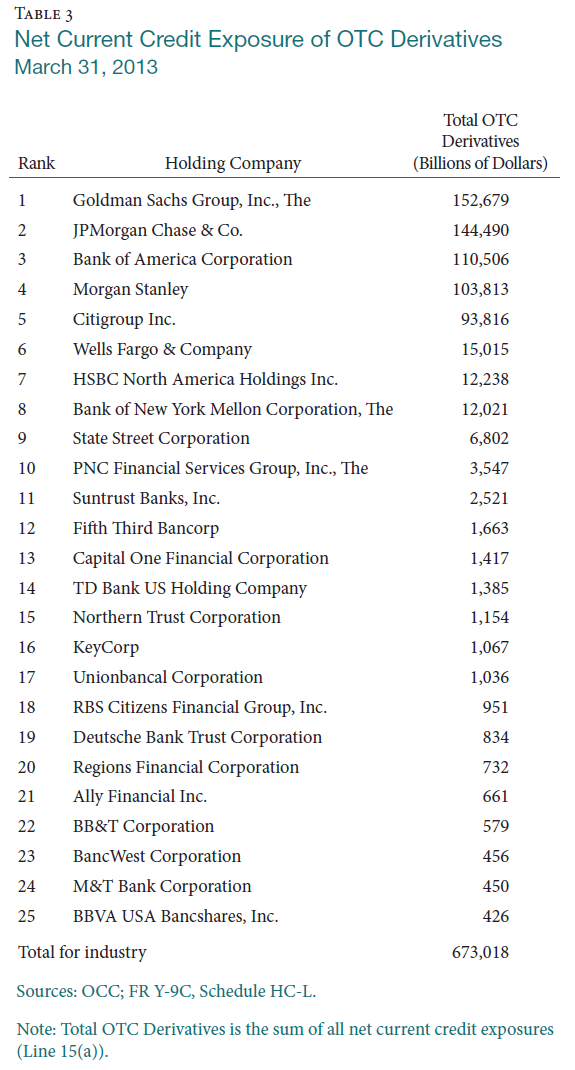

“Five bank holding companies—Bank of America, Citigroup, Goldman Sachs, J.P. Morgan Chase, and Morgan Stanley— represent more than 95 percent of the [U.S.] banking industry’s net current credit exposure for over-the-counter derivatives, which totaled $673 billion in 2013:Q1.”