Large foreign exchange interventions are common in emerging markets, typically in response to capital flows. What is less well understood is the expansionary (contractionary) impact of FX purchases (sales) on local credit, even if the transactions are sterilized. Sterilization securities mostly end up on banks’ balance sheets, where they function as substitutes for bank reserves, serve as collateral, and encourage banks to expand their loans-to-securities ratios.

“Foreign exchange intervention and the banking system balance sheet in emerging market economies”

Blaise Gadanecz, Aaron Mehrotra and Madhusudan Mohanty

IMF Working Papers No 445, March 2014 http://www.bis.org/publ/work445.htm

The below are excerpts from the paper. Emphasis and cursive text has been added.

“Intervention in the foreign exchange market by emerging market economies (EMEs) has been associated with large changes in their banking systems’ balance sheets. As a simple indicator, the aggregate FX reserves of EMEs rose from 16% of GDP in 1997 to 37% of GDP in 2013. Given that banks are the main counterparty in central bank transactions, it is not surprising that their balance sheets have also grown rapidly.”

“The central bank can finance its foreign currency purchases wholly or in part by issuing currency…However, this means of financing is insufficient [and implies an expansionary monetary policy] when foreign currency assets become very large and far exceed the public’s currency holdings. The central bank will then face a financing gap.”

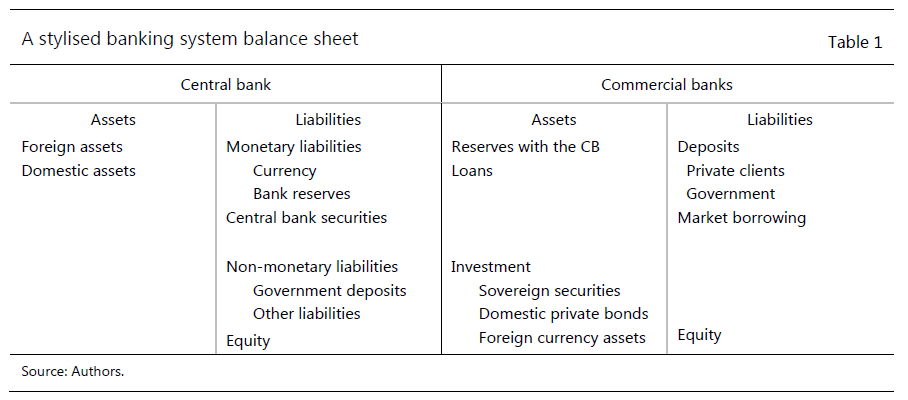

“Following the scheme laid out in [the table above]…one way of financing FX accumulation without increasing bank reserves would be to increase non-monetary liabilities. For instance, the government could be asked to increase its deposits at the central bank …the central bank’s financing gap could also be met by increasing the required reserve ratio on banks…However, the larger and longer-lasting an intervention becomes, the more likely it is to be financed by central bank issuance of securities.”

“The average maturity of securities issued by EME central banks tends to be quite short. In 2011, for instance, close to 85% of central bank securities had remaining maturities of less than a year. Only less than 5% of securities had a maturity of three years or more…The share of banks’ holdings [of sterilization securities] is typically high in all regions, a feature associated with relatively underdeveloped bond markets in EMEs and banks’ strong preference for liquid assets.”

Why sterilized FX interventions still have monetary impact

“Although in the conventional definition of money central bank securities are considered as non-monetary liabilities, they may not be completely neutral from the viewpoint of monetary policy, for several reasons.

- Short-term government and central bank securities can be a close substitute for bank reserves…to the extent that short-term securities yield transaction services and reduce liquidity constraints.

- Investors’ ability to increase leverage may depend on their holdings of liquid government and central bank securities…In particular, given their high collateral values, a high stock of short-term sovereign securities may facilitate increased risk taking in the financial system, leading to higher credit growth.

- Excessive holdings of government bonds are costly to banks as they come at the expense of forgone lending. As a result, banks may reduce their lending rate to reach the desired investment-to-loan ratio. If so, a persistent and significant rise in banks’ holdings of liquid securities is likely to contain information about future lending growth.”

“Even if the central bank holds bank reserves constant, increased holding of short-term liquid securities on commercial banks’ balance sheets may impact bank lending in ways that run counter to the aims of the monetary authority. Such impacts may not be immediate, and could also depend on bank-level characteristics.”

Evidence that how banks’ securities holdings spur lending

“Using country-level data in a panel setup…for a sample of 18 emerging market economies for the period 2001–11 (one country observation per year)…we find that bank holdings of government and central bank paper over time lead to an expansion in credit to the private sector. The effect is strongest in economies with a well capitalised banking system.”

“The estimates with country-level data suggest that when well capitalized banks’ holdings of government and central bank securities, as a ratio of their credit stock, rise by 1 percentage point, their lending growth increases by 0.2 percentage points two years later. This result is economically and statistically significant. Even though it is not the primary factor determining bank lending, this channel accounts for about 16% of the total variance in credit growth during 2001–11.”

“Narrowing down our definition of liquid assets to comprise only short-term government and central bank securities and base money leads to stronger effects. The variance of credit growth explained by liquid assets more than doubles to 37%. Additional estimates using a large data set with bank-level data from BankScope largely confirm these findings.”

“Our results support the ‘impossible trinity’ theory in that FX intervention weakens the monetary authority’s control over domestic monetary conditions. In many EMEs, persistent intervention to resist appreciation has been associated with a highly liquid banking system and strong credit growth. Not only does this bring about difficult trade-offs for EME monetary authorities in setting the appropriate monetary stance, it also creates risks for the financial system.”