Volatility targeting adjusts the leverage of a portfolio inversely to predicted volatility. Since market volatility is predictable in the short run and returns are not this adjustment typically improves conventional risk-adjusted return measures, such as the Sharpe ratio. An empirical analysis for the U.S. equity market over the past 90 years confirms this point but suggests that the real key benefit of volatility targeting is the reduction of outsized drawdowns in extreme market situations. That is because large cumulative losses mostly occur when market volatility remains high for long. On these occasions volatility targeting has benefits somewhat similar to a momentum strategy, selling risk early into market turmoil, thereby positioning for escalation.

Dreyer, Anna and Stefan Hubrich (2017), “Tail Risk Mitigation with Managed Volatility Strategies”.

The post ties in with SRSV’s lecture on risk management, particularly the part on preparing crisis strategies.

The below are excerpts from the paper. Emphasis and cursive text have been added. The terms managed volatility strategies and volatility targeting strategies are treated as synonyms.

What is volatility targeting?

“Managed volatility strategies [strategies based on volatility targeting] adjust exposures in inverse relation to a risk estimate, aiming to stabilize realized portfolio volatility through time.”

“At the heart of…[volatility targeting] lies a well-established and tantalizingly robust feature of financial markets: risk (as measured by volatility) is a time-variant feature of the return distribution, and unlike the expected return, a meaningful share of its time-variation is forecastable by surprisingly simple extrapolation of recently experienced volatility.”

“The most immediate application of this ability to forecast risk is to stabilize realized portfolio volatility. Portfolio volatility stabilization can be accomplished by frequently recalibrating equity market exposure such that the expected portfolio volatility under the forecast aims at a constant target.”

Application to U.S. equity

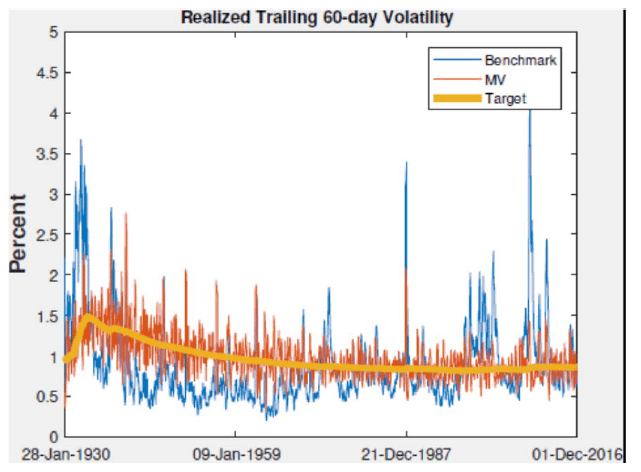

“We focus our analysis on U.S. data only [S&P 500], which allows us to use a very long term sample of daily returns, starting in 1926. One of our key concerns is reliability of findings through time.”

“Managed volatility strategies rely on the ability to forecast near-term risk. As a simple illustration, consider that over our data sample covering U.S. equity market data since 1926, the correlation between adjacent 60 trading day periods is essentially zero for return. In contrast, the correlation rises to 0.55 for risk as measured by standard deviation. Past returns do not predict future returns, but past volatility largely predicts future near-term volatility!”

“We show the rolling realized 60-day volatility for two portfolios: the raw equity market (the static benchmark), and a stylized managed volatility strategy. In our stylized managed volatility strategy, the expected portfolio volatility always equals the long-term target. We achieve this by daily lowering the equity exposure when the volatility forecast exceeds the target and vice versa… The [figure below] clearly shows the volatility stabilization attribute of a managed volatility strategy. The volatility-targeted realized volatility consistently hugs the target volatility within a much tighter range than the benchmark.”

Risk-adjusted returns

“Volatility targeting strategies can and will routinely employ leverage, and feature exposures well in excess of 100% during low volatility episodes. This use of leverage allows volatility targeting to garner excess returns over the benchmark during those low volatility periods, if equity market returns are positive. This opportunity for volatility targeting to ‘quietly’ outperform during calm periods is often overlooked. It is the main feature that can compensate for opportunities lost by de-risking in crisis periods.”

“For a baseline volatility targeting strategy relying on trailing 20-day realized volatility as its forecast, the longest sample starting in 1929 features meaningful Sharpe ratio improvements on the order of 20-30% for holding periods up to a quarter. Consider an investment committee that evaluates performance on a quarterly basis. A quick back-of-the-envelope calculation suggests that at the quarterly frequency, this is comparable to adding an active manager with an annualized tracking error and post-fee information ratio of 3% and 0.5, respectively, something that can certainly not be taken for granted in the active management space, and that many pension committees would look upon quite favorably.”

“Deterioration of the improvement as the holding period lengthens is noteworthy, however… Holding period is the frequency at which the investor scores success (“how often they open their statement”). It corresponds to the window over which individual return observations are cumulated…The analysis confirms the notion that truly long-term investors, ones concerned about performance over holding period beyond one year, and with the necessary behavioral makeup or governance structure to live by that principle, should not expect much of an enhancement from volatility targeting strategies.”

Containment of outsized drawdowns

“Volatility targeting strategies robustly improve the tail risk properties of portfolio outcomes. These outcomes are often not captured by traditional metrics of risk adjusted returns based on the first two moments (average return and volatility).”

“[We calculate] a metric that divides annualized return by the size of “Conditional Value at Risk”…measures of absolute tail risk…These represent the average the bottom 5% and 1%, respectively, of relevant holding period returns. [The ratio] is effectively the tail risk equivalent of the Sharpe Ratio. It replaces volatility as the risk measure with average of the worst outcomes… These metrics [show] robust superiority of volatility targeting strategies regardless of time horizon and sample period… Volatility targeting improves the relevant ratios by 35-50% over the full sample, 15-20% over the sample starting in 1990…We can robustly conclude that volatility targeting strategies have historically provided more return per unit of tail risk than the benchmark.”

“What is the intuition for this impressively robust tail risk reduction feature from volatility targeting strategies? Consider that the tail risk in benchmark returns arises from volatility clustering. The presence of volatility clustering suggests that realized volatility can remain conditionally higher or lower than the average for some time…The same phenomenon that causes fat tails, volatility clustering, is also the key mechanism by which volatility targeting strategies predict volatility, and consequently remove fat tails from the return stream.”

“Volatility targeting strategies invest like momentum strategies, as their dynamic positioning indirectly responds to recent returns….On a simultaneous basis, realized volatility and returns tend to be negatively correlated. The correlation for 60 day windows is -0.25 in our sample, reflecting the simple fact that volatile periods tend to be associated with ‘bad news’ and market selloffs. Since volatility-targeted equity market exposure scales inversely to predicted volatility, largely a function of recently experienced volatility, these dynamics imply that volatility-targeted portfolios tend to reduce exposure subsequent to a selloff.”