The “net stable funding ratio” is a quantitative liquidity standard for regulated banks, scheduled to go into effect in 2018. It will require stable funding sources to be equal or exceed illiquid assets. It may to some degree restrict term transformation of regulated banks and encourage migration into shadow banking. The impact of the new regulation will differ across countries and institutions.

“The Net Stable Funding Ratio: Impact and Issues for Consideration”, Jeanne Gobat, Mamoru Yanase, and Joseph Maloney

IMF Working Paper, 14/106, June 2014

http://www.imf.org/external/pubs/cat/longres.aspx?sk=41648.0

The below are excerpts from the paper. Cursive text and underscores have been added.

The background

“Liquidity risk [in banks] arises on both sides of the balance sheet: if either the liquidity generated from selling liquid assets, or from securitizing assets, or the liquidity available from various funding sources is insufficient to meet cash obligations as they fall due. Maturity transformation inherently exposes banks to investor and/or deposit runs, with implications for bank solvency and bank survival.”

“Under its new international regulatory framework for banks, known as Basel III, the Basel Committee on Banking Supervision (BCBS) issued two quantitative liquidity standards in 2010—the Liquidity Coverage Ratio (view post here) and the Net Stable Funding Ratio (NSFR). It is the first time that the BCBS is requiring liquidity risk standards to be implemented consistently across jurisdictions.”

The definition

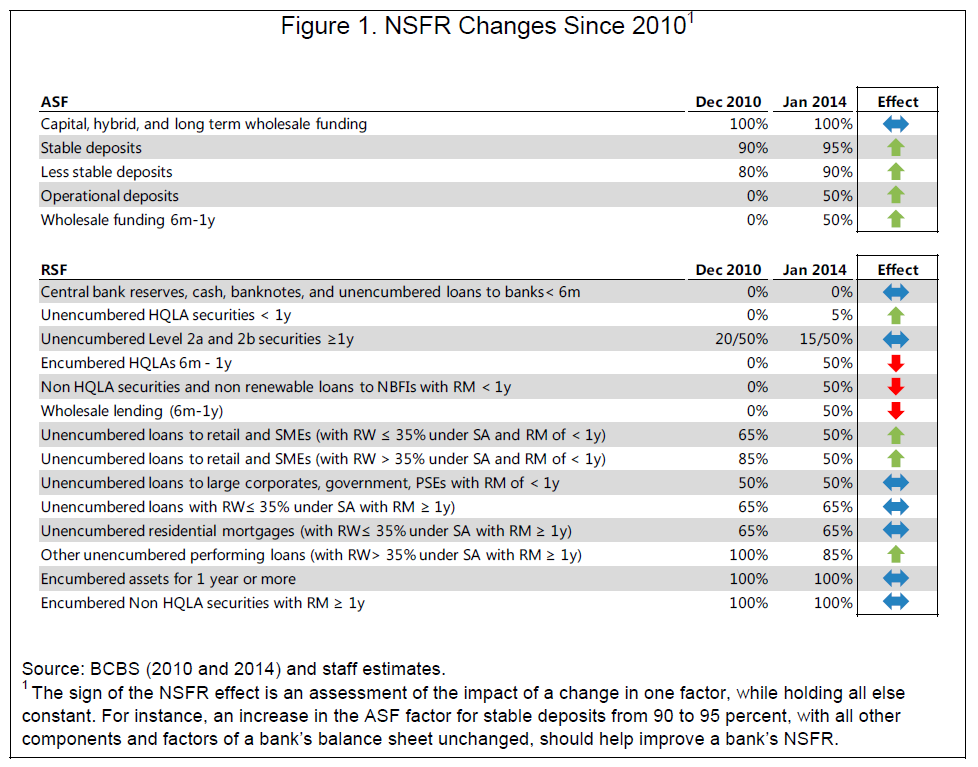

“The NSFR…is defined as a bank’s available stable funding (ASF) divided by its required stable funding (RSF), with banks having to meet at minimum a regulatory ratio of 100 percent beginning 2018. ASF is the portion of a bank’s funding structure that is reliable over a one year time horizon, while the RSF is the portion of a bank’s assets and off balance exposures that are viewed as illiquid over a one year horizon.”

“The ASF and RSF weights range from 100 percent to 0 percent to reflect the stability of funding for liability categories and the liquidity of asset categories. A higher ASF weight is attached to more stable funding. For example, regulatory capital enjoys a 100 percent ASF weight while stable non-maturity deposits receive a 95 percent ASF weight. In contrast, funding from a financial institution with residual maturity less than six months has a 0 percent ASF. Similarly, liquid assets enjoy lower RSF factors while illiquid assets are assigned higher RSF factors. Central bank reserves have a 0 percent RSF weight and performing loans are assigned a 85 percent RSF weight.”

The purpose

“The NSFR, which is expected to go into effect in January 2018, aims to encourage banks to hold more stable and longer term funding sources against their less liquid assets, thereby reducing maturity transformation risk.”

“Broadly, the NSFR aims at discouraging certain banking practices that are considered financially unsound, including excessive liability and asset concentrations and mismatch, and lowering reliance on instruments that are highly volatile and pro-cyclical. The NSFR should help discourage banks’ over-reliance on short-term wholesale funding (less than one year) and encourage greater mobilization of stable sources such as deposits or bond market financing, or even capital. In its calibration and intent, the NSFR takes on many aspects of traditional industry liquidity risk management practices, including balance sheet liquidity analysis and cash capital position.”

The impact

“The main arguments against the NSFR are that:

- it may be too restrictive and undermine banks’ traditional role in liquidity and maturity transformation, and could lead to a shortage in long-term lending with real consequences for economic growth;

- it could make deposits less stable as banks compete for this scarce funding source;

- it may encourage maturity transformation activities to migrate to the ‘shadow banking’ sector and hence not address systemic risk;

- it could have a more severe impact on emerging markets and developing economies (EMDEs), which tend to have less developed capital markets and rely more on banks for long-term financing;”

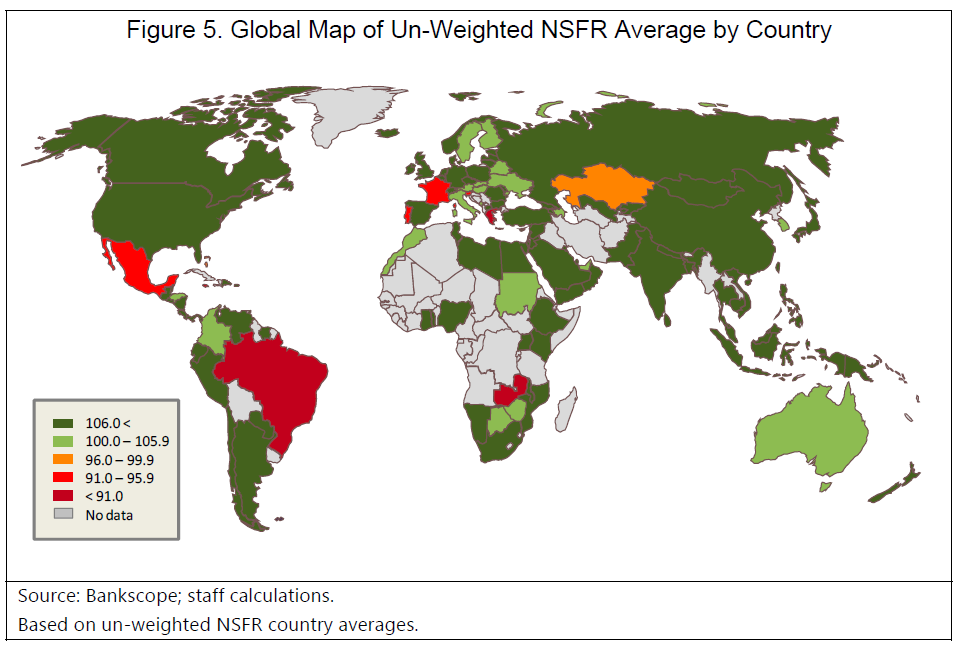

“Most banks in Asia and some advanced countries, such as the United States, appear to have sufficient funding buffers to meet the NSFR minimum threshold by early 2018 without requiring significant adjustments to their balance sheet. By contrast, the transitional costs will be higher for countries with larger gaps, in particular if their systemically important banks have a shortfall. This includes some advanced countries such as Australia, France Italy and Sweden as well as large [emerging economies]…such as Brazil, Mexico, Ukraine and Russia.”