Galsband and Nitschka claim that the outperformance of high-carry currency trades over the past 30 years reflects a premium for correlation with shocks to equity cash flows. While the finding may sound trivial, its implications are important. In particular, in connection with the negative impact of currency strength on local equity, the fx carry-equity nexus would imply that carry countries’ local-currency equity returns should outperform in crisis times, as they are buffered by the exchange rate and become a better diversifier, when all other correlation increase.

Foreign-currency returns and systemic risks

Victoria Galsband, Thomas Nitschka, 10 March 2013

http://www.voxeu.org/article/foreign-currency-returns-and-systemic-risks

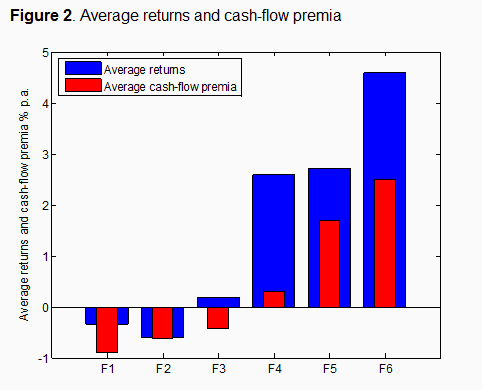

“At least since the 1980s..borrowing in low-interest-rate currencies and investing in high-interest-rate currencies promises a positive return…The same logic applies to high versus low forward-discount currencies. [The figure below] plots the average annualised returns on six-monthly rebalanced forward discount-sorted currency portfolios over the sample period, from December 1983 to December 2010. The portfolios are constructed in such a way that portfolio ‘F1’ always consists of the lowest forward-discount currencies, while portfolio ‘F6’ always contains the highest forward-discount currencies…A simple investment strategy which takes a long position in ‘F6’ and a short position in ‘F1’ promises roughly 5% per annum on average!”

“There is a tight link between equity and foreign-exchange markets…currencies that appreciate when the stock market falls might be a good investment since they provide a valuable insurance against unfavourable fluctuations on equity markets. On the other hand, currencies which depreciate in times of poor stock-market performance tend to further destabilise investors’ positions and should hence offer a premium for their risk. We find strong empirical support for our hypothesis.”

“Campbell and Vuolteenaho (2004)…point towards two sources of systematic risk in equity markets. The first is ‘bad’ long-lasting cash-flow news about…dividends. The second is ‘good’ short-lived news about future-market rates applied to discount these cash flows…We document a strong relation between currencies’ average returns and their sensitivities to cash-flow shocks in equity markets. High forward-discount currencies react strongly to stock-market cash flows while low forward-discount currencies are much more resilient in this regard… Depending on specification, our model can explain between 81% and 87% in total variation in average returns on foreign-currency portfolios”