Sovereign wealth funds now hold assets worth roughly 4% of global GDP, and are governed by politically-mandated investment objectives. A new IMF paper gives an overview of size, types, investments and governance structures of these institutions.

Sovereign Wealth Funds: Aspects of Governance Structures and Investment Management

Abdullah Al-Hassan, Michael Papaioannou, Martin Skancke, and Cheng Chih Sung

IMF Working Paper 13/231

http://www.imf.org/external/pubs/ft/wp/2013/wp13231.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

The size of Sovereign Wealth Funds

“Sovereign wealth funds (SWFs) are special purpose investment funds or arrangements that are owned by the general government. Created…for macroeconomic purposes, SWFs hold, manage, or administer assets to achieve financial objectives, and employ a set of investment strategies that include investing in foreign financial assets.”

“Total assets under management by Sovereign Wealth Funds (SWFs) have been growing rapidly over the last few years…Upper-end estimates indicate total SWF assets of around USD5 trillion. This figure, however, may double count some sovereign assets, by including central bank assets that are already captured in official reserves. Based on the definition of the International Working Group of Sovereign Wealth Funds, which excludes central banks and state-owned enterprises, the total assets of SWFs—with publically available data for thirty SWFs—are about USD3 trillion [4% of global GDP].”

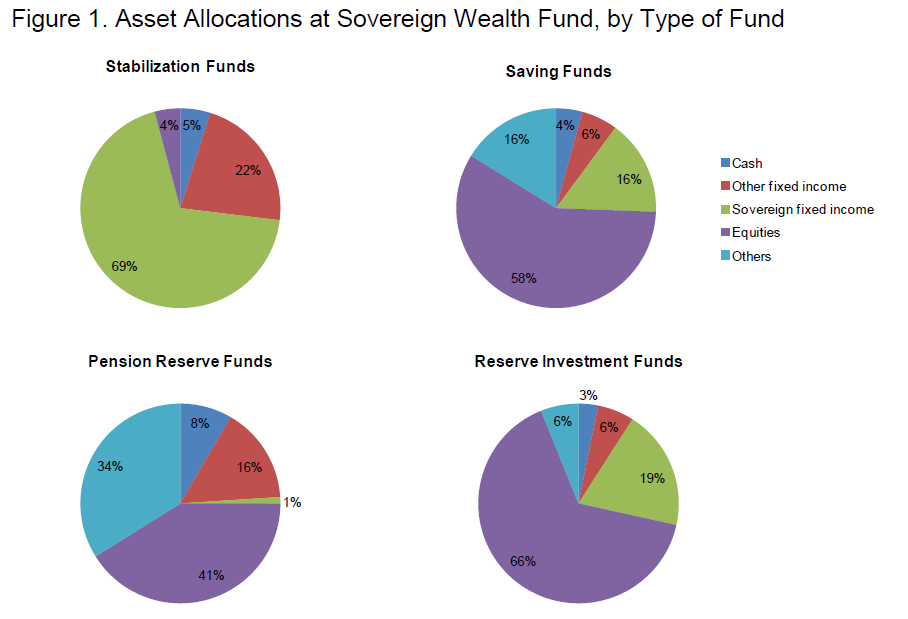

The types of Sovereign Wealth Funds

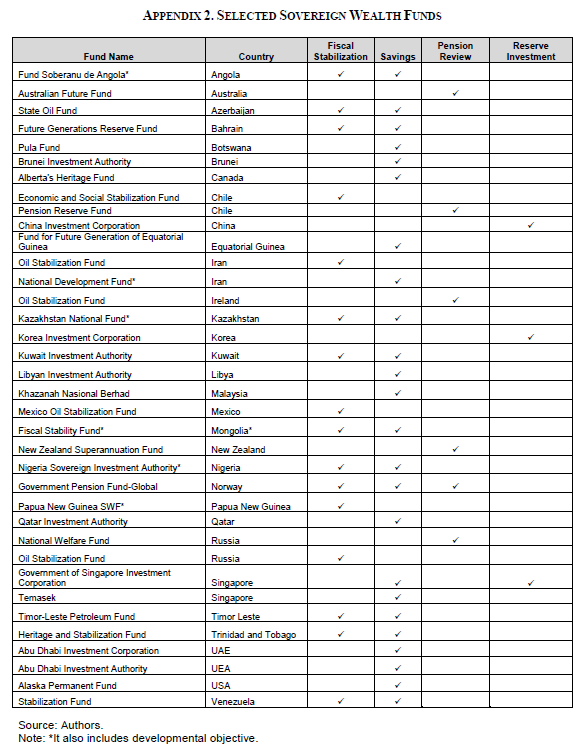

- Stabilization funds are set up to insulate the budget and economy from commodity price volatility and external shocks…[Examples are] Chile (Economic and Social Stabilization Fund), Timor-Leste, Iran, and Russia (Oil Stabilization Fund). Their investment horizons and liquidity objectives resemble central banks…They tend to invest largely in highly liquid portfolio of assets by allocating over 80% of their assets to fixed income securities, with government securities consisting around 70% of total assets.

- Savings funds intend to share wealth across generations by transforming non-renewable assets into diversified financial assets…[Examples include] Abu Dhabi Investment Authority, Libya, and Russia (National Wealth Fund). Their investment mandate emphasizes high risk-return profile, thus, allocating high portfolio shares to equities and other investments (over 70%).

- Development funds are established to allocate resources to priority socio-economic projects, usually infrastructure…[Examples are] the United Arab Emirates (Mubadala) and Iran (National Development Fund).

- Pension reserve funds are set up to meet identified outflows in the future with respect to pension-related contingent-type liabilities on the government‘s balance sheet [for example in] Australia, Ireland, and New Zealand. They held high shares in equities and other investments to offset rising pension costs.

- Reserve investment corporations intend to reduce the negative carry costs of holding reserves or to earn higher return on ample reserves, while the assets in the funds are still counted as reserves…[Examples are] China, South Korea, and Singapore. To achieve this objective, they pursue higher returns by high allocations in equities and alternative investments—with up to 50% in South Korea and 75% in Singapore‘s Government Investment Corporation.”