The IMF Article IV consultations for the U.S. suggest that a Federal Reserve exit from unconventional and highly accommodative policy may be challenging. Most importantly, quantitative estimates and past experiences indicate that the term premium on long-dated bond yields can vary greatly and become disruptive for markets and the economy. Meanwhile, the envisaged “passive” rundown of large treasury and MBS holdings would take a long time to unwind the Fed’s bloated and more risky balance sheet. And as long as excess reserves are ample even the Fed’s control over short-term rates will be imperfect.

Exiting from unconventional monetary policy: potential challenges and risks.

United States – Article IV Consultations – Selected Issues, July 26, 2013

http://www.imf.org/external/pubs/cat/longres.aspx?sk=40828.0

The below are excerpts from the report. Cursive text and emphasis have been added.

The main point

“Ensuring an orderly exit from ultra-accommodative monetary conditions is likely to be accompanied by a range of operational and other policy challenges…[i] containing abrupt, sustained moves in long-term interest rates; [ii] managing an effective pass-through from policy tightening to short-term market rates; and [iii] coping with potential balance sheet losses.”

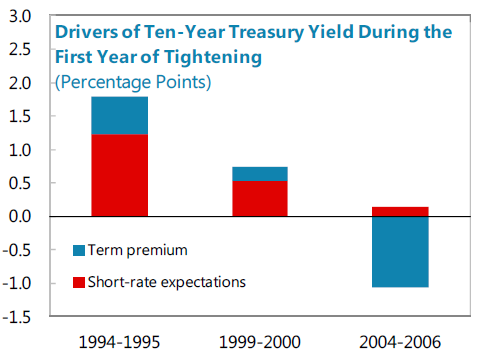

Risks related to the bond market term premia

“Long-term bond yields behaved differently during recent episodes of monetary tightening, largely due to different responses in the term premium. The 1994-1995 tightening episode―which saw policy rates rise 300 bps over a 13-month period―was accompanied by a substantial increase in the term premium, reflecting concerns among bond investors over inflation and a lack of policy transparency from the Fed…During the 1999–2000 episode, when policy rates rose by a more modest 175 bps over a similar timeframe as in 1994–5, there was a more subdued rise in the term premium. In contrast, the 2004–06 cycle, which saw policy rates rise by 425 bps in 25 bps increments over a two-year period, was accompanied by a substantial decline in the term premium, arguably leading to a somewhat more accommodative policy stance than intended by the Fed. ”

“A rapid change in the term premium might complicate the exit from QE and normalization of monetary policy. Various factors could potentially exert sudden upward pressure on the term premium in the forthcoming cycle, including, for instance, uncertainty about the U.S. or global economic recovery and inflation outlook or general policy uncertainty as the Fed seeks to re-normalize monetary policy conditions.”

“We explore the statistical relationship between the ten-year term premium…and a set of variables closely associated with its movement… including changes in macroeconomic fundamentals, macro uncertainty, financial market volatility, and changes in the Fed’s LSAP [Large-Scale Asset Purchase] program…The model estimation suggests that term premia are closely related to macroeconomic fundamentals, in particular labor market conditions, financial market volatility, and unconventional monetary policy measures as well as uncertainty on future policy actions. Term premia are countercyclical, increasing when the unemployment rate, financial market volatility, or monetary policy uncertainty rise. An expansion in the Fed’s holdings effectively lowers the term premium.”

“Estimation results suggest that…between September 2008 and March 2013:

- Changes in market expectations of the Fed’s balance sheet size caused by the various LSAP programs and forward guidance announcements lowered the ten-year term premium by about 100 basis points.

- Reduced financial market volatility and near-term short-rate uncertainty since late 2008 helped lower the term premium substantially, by more than 70 basis points;

- Changes in macroeconomic fundamentals…increased the ten-year term premium by 30 basis points, largely due to an increase in the unemployment rate;

- Declines in macroeconomic volatility had a negligible effect on the term premium, amounting to only 10 basis points.”

“Events that lead the market to expect an earlier unwind of the LSAP may also trigger a change in the expected timing of short-term rate increases, thereby driving 10-year bond yields higher. A simple calculation suggests that expectations of an earlier federal funds rate “lift-off” of two quarters may increase the ten-year bond yield by at least 25 basis points. Changes in market sentiment may also be accompanied and further reinforced by heightened financial market volatility. In our…scenario (“Rush to Exit” in the midst of heightened policy uncertainty and market volatility), higher financial market volatility leads to an additional 40 basis point increase in the ten-year term premium, resulting in an overall jump in the term premium of almost 100 basis points and an increase of more than 125 basis points in ten-year Treasury bond yields. The magnitude and persistence of such increases would be comparable to those of Greenspan’s “long-term bond yield conundrum” during 2004–2006―but in reverse―and would likely generate pervasive effects on the U.S. economy and global financial markets.”

The Fed may need to run a large and more risky balance sheet for long

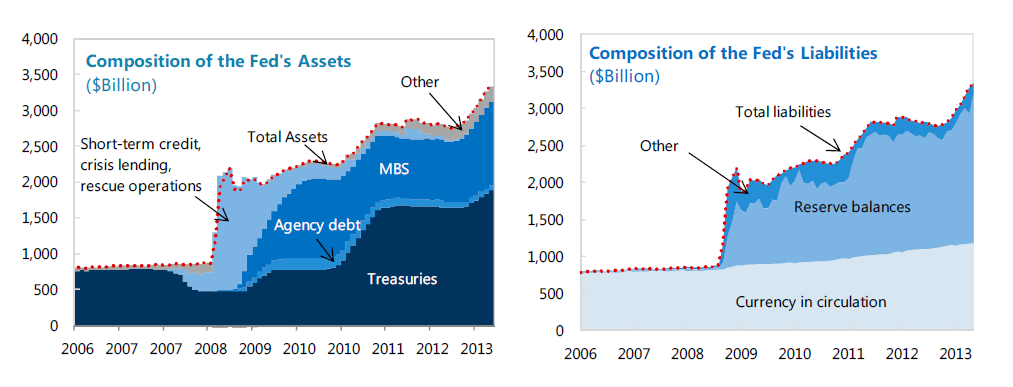

“At just over USD3 trillion, the Fed’s balance sheet is already more than twice as large as it was before the financial crisis . The composition has also changed. Pre-crisis, the portfolio was comprised almost exclusively of Treasury securities more or less consistent with the maturity distribution of the stock of outstanding marketable Treasury securities and liabilities mostly comprised of costless currency in circulation. Currently, assets include a mix of Treasuries, agency mortgage-backed securities (MBS), as well as agency debt. The overall duration of the portfolio is also longer, partly due to Operation Twist (whereby the Fed sold short-term securities from its portfolio and bought long-term securities), while liabilities are dominated by bank reserves on which the Fed pays interest.”

“The Federal Open Market Committee (FOMC)…planned exit strategy…entails the following steps:

- First, the Fed plans to cease reinvesting principal payments.

- At the same time or sometime thereafter, the Fed intends to modify its forward guidance [on interest rates] and start draining reserves.

- Then, the Fed plans to raise the fed funds target and increase the IOER [interest on excess reserve balances introduced in 2008] as needed, while continuing to allow securities in its portfolio to mature.

- The committee had expected to start unwinding its portfolio via outright sales of agency debt and agency MBS sometime thereafter over a 3–5 year period. But [in 2013] the Fed has put less emphasis on asset sales, owing to concerns about market disruptions (view post here).”

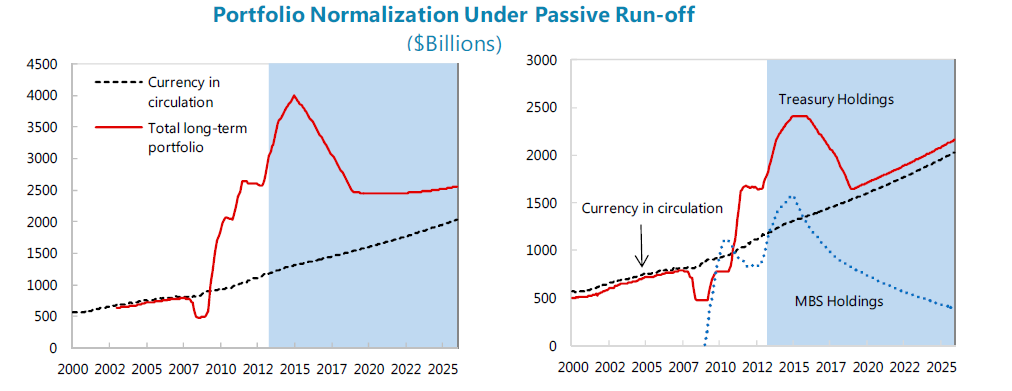

“In principle, it is possible for the Fed to allow its portfolio to shrink exclusively through passive run-off, but it will take a long time for the overall portfolio to normalize both in terms of size and composition. Assuming that QE-related purchases continue through June 2014, it would likely take about five years for the treasury portfolio to revert to its historical norm. Based on this simulation, the duration of the portfolio will remain above the historical average for some time. The MBS portfolio will take much longer to wind down if the Fed relies only on passive pay-downs, since prepayment speeds will likely slow as interest rates rise. Even under aggressive assumptions for prepayment speeds, the MBS portfolio will likely take roughly 30 years to fully run off.”

With large excess reserves control over the Fed Funds rate is imperfect

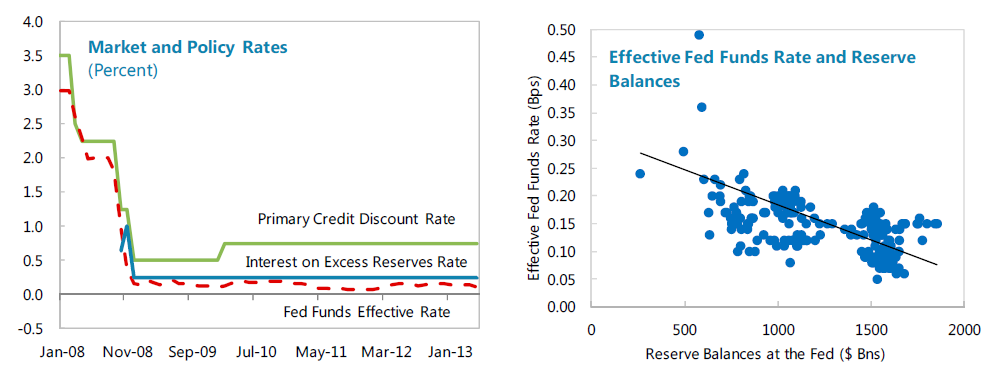

“The effective fed funds rate has remained below the IOER since its inception. This means that some institutions effectively lend funds at a rate below that paid by the Fed. This is partly because not all participants are eligible to receive interest on their reserve balances. The GSEs [Government Sponsored Enterprises, such as Fannie Mae], in particular, which are significant lenders of cash in the fed funds market, are not eligible to receive interest on balances held with the Fed. At the same time, the Fed’s LSAP [Large-Scale Asset Purchase] programs have led to a steady increase in excess reserve balances, in turn reducing interbank trading volumes (since a primary reason for banks to borrow fed funds is to ensure that they maintain sufficient reserves)… Fed funds effective trading volumes were around USD250 billion pre-crisis and have fallen to approximately USD50 billion per day currently.”

“Prior research (Bech and Klee, 2009) suggests that in an environment of elevated excess reserves, the pass-through from a rise in the IOER to the effective fed funds rates may be less than 1 to 1. To keep the effective fed funds rate near the FOMC’s target rate, the Fed may need to drain a large volume of reserve balances”