In a short note Macquarie’s commodity research reviews price distortions and prospective changes related to the warehouse system of the London Metals Exchange (LME). Since 2008 LME warehouses have effectively withdrawn over 4 million tons of aluminium from the physical markets, producing a record premium for physical delivery versus exchange spot prices. Premiums have also climbed for other metals. A future increase in mandatory load-out rates could compress premiums but also adds to uncertainty about the resulting adjustment in exchange prices.

Bazooka!! – Macquarie Commodities Comment – July 2, 2013

(Proprietary research without public link. Please contact Macquarie Capital for access)

The theory of metals prices

“In principle the natural shape of the forward price curve for any non-perishable commodity, such as LME-traded metal, is a contango (forward price > cash price) equal to the cost of ‘carry’ – that is, the cost of holding stocks, namely financing, storage and insurance. The forward price is not a forecast. Where a contango is less than cost of carry, or more obviously where a forward price curve is in backwardation (cash price > forward price), there is an incentive to sell promptly and reduce stocks.”

“The physical premium for LME-traded metals is the amount over and above the exchange price a buyer is prepared to pay for the physical purchase and possession of metal in a particular location…In principle the premium is to cover suppliers’ costs in physically providing metal to the buyer…Historically, premiums have typically amounted to only a small proportion of the exchange price and in times of surplus, as in most metals markets today, it might intuitively be thought that premiums would be low.”

The reality at the London Metals Exchange

“[However] more and more metal [is] being jammed into fewer and fewer [warehouse] locations in the context of limited load-out rates [capacity to take stocks out of a warehouse]… LME minimum load-out rates become de facto market maximums since warehouses are in the business of holding metal in storage in return for rental income… [Also] money has been very cheap for many years and metal market surpluses have tended to keep forward price curves in contango [making warehouse storage and forward selling profitable]. This confluence of factors has limited consumer access to metal stocks in some circumstances…and inflated physical premiums for metals, which has further encouraged financial investors to accumulate inventory in a self-reinforcing feedback loop.”

“The way in which more and more metal has piled up in fewer and fewer locations is most apparent in the aluminium market, and the impact can be illustrated by way of a simple hypothetical example… imagine 30,000 tonnes of aluminium in stock. If this is distributed evenly across ten warehousing company locations it could be returned to the market with in one-to-two days at current minimum load out rates. In contrast, it is all held in a single warehousing company location it would take between 20 and 40 days to return to the market. This has important implications for consumer access to metal in storage, if only from a practical perspective (a long wait for a just-in-time manufacturer may not be practical) and for the potential rental value of each additional metal unit to a warehousing company.”

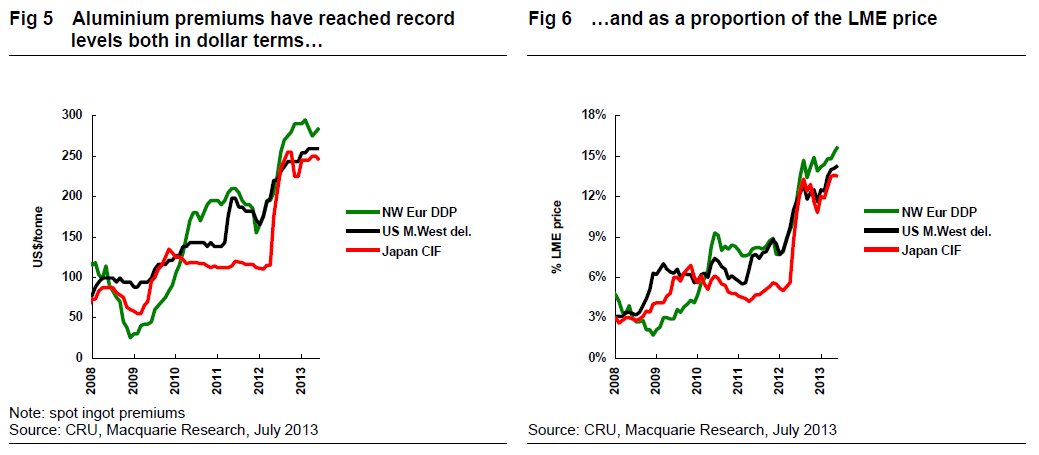

“Most obviously, and most controversially for some consumers, physical premiums for aluminium have been bid up to all-time record levels, both in dollar terms and as a proportion of exchange prices Premiums have substantially outperformed exchange prices and premiums for LME deliverable products have performed best (since these are most easily financed and so most in demand). Premiums for other metals have also been rising steeply.”

“This inflation of premiums relative to the LME price has a number of important implications. It complicates the task of price risk management since premium risk cannot be hedged as easily or effectively as exchange price risk and the higher the proportion of the total price represented by the premium the more of a potential problem this becomes. It also potentially distorts input and/or output markets priced in relation to the LME price… some consumers are appear to have been left feeling overcharged for metal by way of elevated premiums at a time when the market is in surplus and stocks at record highs. It is outcomes such as these that have left the LME aluminium price looking broken to some market stakeholders.”

Prospective changes

“It is in the context of such concerns about the credibility of LME metals prices that the LME has launched its consultation on a proposal that it says specifically is ‘designed to cut warehouse queues’. The consultation is open from 1st July to 30th September and a final decision on whether to implement any change(s) will be made at a scheduled board meeting in October. Any changes confirmed at that time would then take effect from 1st April 2014. Officially, the LME is open-minded on the issue but we think it highly unlikely that it would ultimately decide to continue with the status quo.”

“At its core the [proposal] is aimed at warehousing company locations where there are queues to withdraw metal of over 100 calendar days…In terms of mechanics, where queues are exceed the above threshold, warehousing companies would be required to load out at least 1,500tpd more metal than delivered in. Additionally, if the current load-in rate of an affected warehousing company location exceeds the minimum load-out rate then that same warehousing company location would be required to deliver out tonnage equal to that excess.”

“As a result, physical premiums would probably trend down in the long run because a warehousing company’s scope would afford incentive payments as a function of the length of time it could be sure of metal remaining in storage would be reduced… Since premiums are plainly at risk of falling, the appetite among financiers for so-called ‘carry’ trades might now be diminished, at least until the potential implications of change have been more fully digested.”