A new paper estimates that U.S. economic data explain more than a third of bond price fluctuations on a quarterly basis. The economic data impact on daily fluctuations is much weaker. It grows with the time horizon because economic factors are more persistent than non-fundamental factors. The simple powerful message is that economic news flow is crucial (and probably underestimated) for identifying market trends.

Altavilla Carlo, Domencio Gianonne, and Michele Modugno (2014), “Low Frequency Effects of Macroeconomic News on Government Bond Yields”, ECARES Working Paper 2014-3

https://dipot.ulb.ac.be/dspace/bitstream/2013/174573/1/2014-34ALTAVILLA_GIANNONE_MODUGNO-low.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

The design of the research

“We analyze the reaction of the U.S. Treasury bond market to innovations in macroeconomic fundamentals… The sample period is January 1, 2000 to January 28, 2014….We identify innovations in macroeconomic fundamentals based on macroeconomic news, which we define as the differences between the actual macroeconomic releases and the median market predictions by participants for those releases. Our analysis is based on the regression of the daily changes in bond yields on macroeconomic news, in the same manner as event studies. The fit of the regression and the corresponding residuals are defined as the fundamental and non-fundamental components of bond yield changes, respectively.”

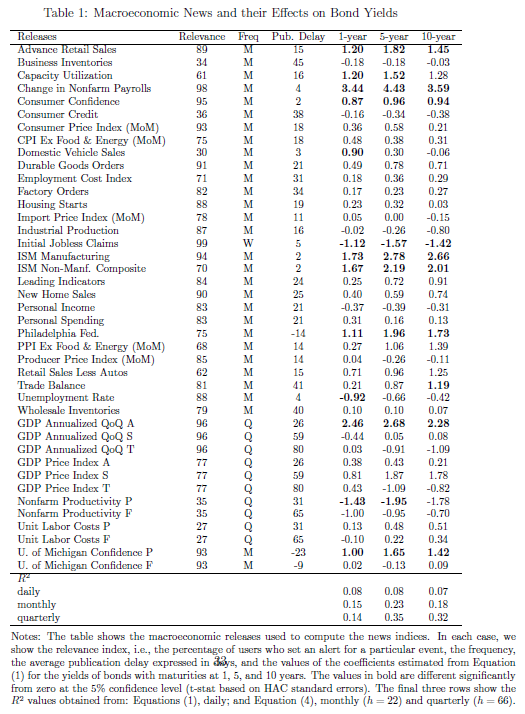

“We use…the Economic Calendars (ECO) provided by Bloomberg. For each macroeconomic release, this dataset contains the realized value and the predictions made by a panel of market participants for the same value…The survey value used in the empirical analysis is the median (consensus) forecast. Using both the official releases and the corresponding forecast for each macroeconomic variable allows us to reconstruct the size and direction of all news that hit the market at each point in time… [The news are matched with a] relevance index. The value of this index corresponds to the percentage of Bloomberg users who set an alert for a particular event.”

The daily impact of economic news

“Focusing on high frequency changes can facilitate the correct identification of the causal effects of macroeconomic news by reducing the effects of confounding factors… we regress the daily change in a bond yield…on day t on a constant and on the news released on day t… In agreement with previous studies, we find that several types of macroeconomic news are economically important and they have statistically significant impacts on daily changes in bond yields. However, their explanatory power is quite limited, i.e., the R2 value of the regression [the ratio of fluctuation explained on a daily basis] is about 10% only.”

“Three groups of variables are particularly important for explaining the daily changes in yields throughout the whole maturity spectrum: surveys (consumer confidence, ISM manufacturing and non-manufacturing, Philadelphia Fed. economic outlook, and University of Michigan Confidence preliminary), employment-related variables (change in nonfarm payrolls and initial jobless claims), and other macroeconomic variables (e.g., GDP annualized QoQ advanced and advanced retail sales).”

The monthly and quarterly impact of economic news

“To analyze the persistence of the effects of macroeconomic news on yield changes, we aggregate the yields and news indices over different time spans. Specifically, we aggregate the daily changes in bond yields to obtain longer horizon changes. Similarly, we sum the daily news indices to obtain longer horizon news indices at daily frequencies.”

“By summing the fit of the daily regressions over a month (quarter), we obtain the fit for the monthly (quarterly) changes in bond yields. The fundamental component becomes more important when focusing on these low-frequency changes; indeed, moving from daily to quarterly increases the [ratio of fluctuations explained by macroeconomics news] …to over 30%. This is because macroeconomic news has a persistent effect on bond yields, whereas the effect of non-fundamental factors is less persistent and it tends to average out when focusing on longer horizon changes. In other words, the importance of macroeconomic factors is hidden by the high frequency noise that dominates the daily fluctuations in bond yields.”

“The types of macroeconomic news considered in this study are only a subsample of the innovations in macroeconomic fundamentals that may affect U.S. Treasury yields. We do not consider surprises related to policy announcements regarding monetary and fiscal policy interventions. Moreover, we only consider U.S. variables, but international factors could also have played important roles.”

The impact of economic news at the zero lower bound for rates

“Interestingly, the interaction between macroeconomic news and yields did not break apart after the zero lower bound became binding at the end of 2008…we show that macroeconomic news continued to exert an important influence at a low frequency on changes in bond yields. This evidence corroborates the view that the non-standard monetary policies adopted by the U.S. Federal Reserve, i.e., a combination of forward guidance and large-scale asset purchases, have been successful in keeping the bond yields anchored to macroeconomic news.”