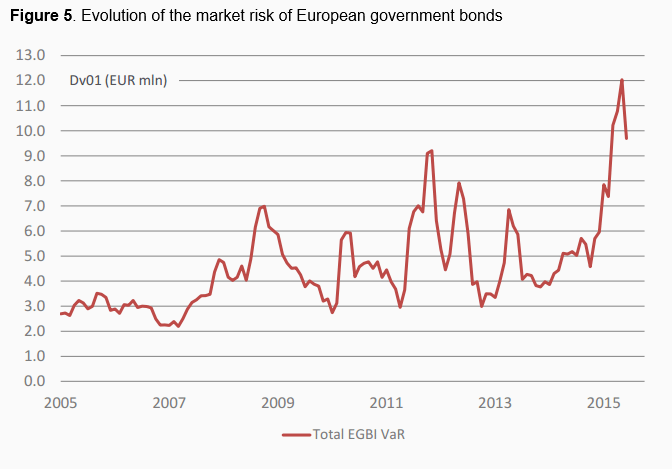

There are signs of liquidity decline and liquidity illusion in euro area government bond markets. Citibank research suggests that liquidity risk is rising due to increased capital requirements for dealers, reduced market maker inventories, enhanced dealer transparency rules, elevated assets under management of bond funds, and the liquidity transformation provided by these funds.

Regesta, Matteo and Alessandro Tentori (2015), “Market liquidity in liquid markets: Pitfalls and trends”, VOX portal, 04 October 2015

http://www.voxeu.org/article/market-liquidity-liquid-markets-pitfalls-and-trends

Regesta, Matteo and Alessandro Tentori (2015), “The Market for Euro Government Bonds: Trends in Liquidity Conditions and Market Micro-Structure”, Citi Research, 7 September 2015.

(please contact Citibank for access to this paper)

The below are excerpts from the post and paper. Headings and cursive text have been added.

For a basic introduction to market liquidity risk view post here.

For general points on the development of bond market liquidity risk in recent years view post here.

European fixed income liquidity decline and liquidity illusion

“Over the past 10 years, the notional value of the iBoxx Eurozone sovereign index has increased by 60% with the number of bonds in the index increasing by 36%. The average issue size has improved from EUR 12.5bn to EUR 14.8bn, probably reflecting more frequent taps of existing lines, both on- and off-the-run. Furthermore, the size of the EGB [European government bond] market has also increased relative to the size of the economy.”

“Liquidity reflects the probability of a transaction taking place at the desired time, at the desired price and in the desired size without disrupting market pricing…There is no guarantee that large and frequently trading markets will stay liquid under all circumstances.”

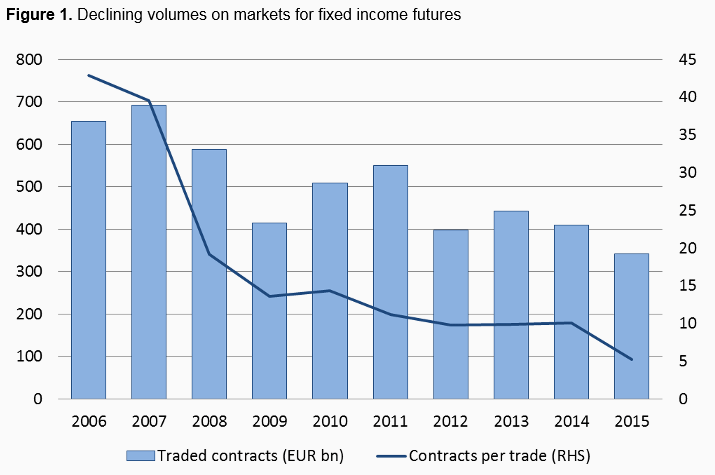

“Liquidity in markets for liquid fixed-income securities…has been on a declining trend for some time. For example, both traded volumes in Eurex fixed-income products and the number of contracts per trade have been on a long-term declining trend… Activity in EUR-denominated fixed income futures has declined further in 2015”

“Bid/ask spreads on electronic markets don’t seem to have widened particularly despite the increase in delivered volatility.. We get a similar picture by looking at electronic EGB bid/ask spreads across countries. However, this picture of EGB liquidity might be distorted by the lower average size that is executable at these spreads. This is sometimes referred to as ‘liquidity illusion’. Anecdotal evidence suggests that the average ticket size has declined.”

“We suspect that if this trend continues, ticket sizes for cash EGBs will shrink to meaningless levels…and the next step might be a pronounced widening of liquidity spreads, a bifurcation of liquidity between benchmarks and off-the-run vintages or between risk-free rates and other asset classes, as well as a more frequent ‘spraying’ of trades across market-makers.”

On recent recurrent signs short-term distress and vanishing liquidity in large developed markets also view post here.

Factors of rising liquidity risk

“We find that several forces might be having a negative effect on liquidity conditions:

- According to the UK Department for Business, Innovation and Skills, we are already seeing the negative effects of regulation on fixed-income markets, that is, a declining allocation of capital to market-making activities and a reduction of inventories… the size of the bond inventory determines the risk of a delay in a market-maker’s risk processing, which ultimately leads to a higher discount required to keep the market in equilibrium…

- Trade transparency rules [in the wake of Markets in Financial Instruments Directive 2 or MiFID2] …matter not only for end investors, but also for market makers who ultimately provide liquidity to markets. Disclosing a transaction in an illiquid security exposes the dealer to liquidity risk in addition to market, credit and operational risks. Hedging liquidity risk is always problematic and often even impossible. The dealer’s rational response might vary from not quoting at all to maximising the bid/ask spread, reducing the trade size or a combination of the above…

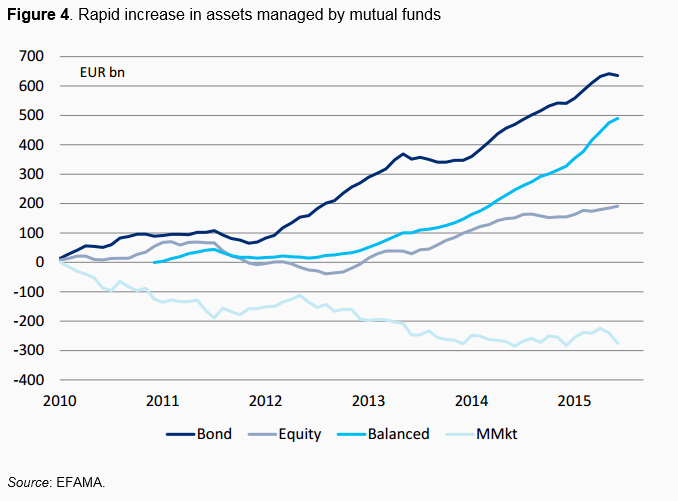

- The European investment fund industry has seen a stellar growth in assets-under-management since 2012 (ring-fencing of sovereign risk): Total…assets have increased by EUR 3.6 trillion (65%) from Dec-11 and by EUR 4.6 trillion (102%) from pre-crisis levels. Relative to 2011, sizeable growth has come from bond funds (EUR 566bn) and balanced funds (EUR 475bn)…The importance of fund managers as ‘T+1 liquidity providers’ should not be underestimated. The liquidity transformation function of the asset management industry could become a systemic issue in case of large and fast redemptions. In theory, investors who invest in mutual funds have also purchased an embedded liquidity option – the fund manager has a skew towards investing in less liquid instruments, while at the same time providing quasi-ready liquidity to his investors…

- From a global cross-industry perspective, there has been a clear divergence between asset manager and bank revenues. Since 2006 sell-side revenues have fallen by 20% (USD 55bn), whereas buy-side revenues have risen 45% (USD 135bn)…as quantitative easing translated into strong asset growth benefiting asset managers”. At the same time, liquidity provision by asset managers has also increased rapidly with more than 45% of global assets-under-management being reported as ‘daily redeemable’.”

On the surge in the euro area investment funds industry, the related surge in the shadow baking system and the resulting pro-cyclical market liquidity risks also view post here.

On the feedback loop between liquidity and government bond collateral value view post here.

The consequences of liquidity risk

“Liquidity risk gives birth to one of the paradoxes of regulation in fixed-income markets – the aim for more transparency might depress market liquidity and distort the price-finding process, with the ultimate collateral cost of reducing transparency. Fixed-income markets mainly differ from equity markets in terms of the number of securities per issuer and the resulting fragmentation and bifurcation – the splitting in two – of liquidity.”

“A protracted structural shift toward less liquid EGB markets might have consequences for the vast majority of existing investment strategies, whose common factor is the ‘short vol’ approach.”

“In order to process both new and existing risk, which is already at historical highs, market makers rely on customer flows (agency model) as well as on their risk limits (principal model). The ability to trade liquid instruments is essential for the hedging of large bond flows in a quote-driven market. If the regulator reduces the number of [market makers] or fully prohibits principal trading, thus limiting dealers’ aggregate risk-processing capacity, then we might face the risk of congestion resulting in wider bid/offer spreads, lower liquidity and eventually higher yields.”

“The term structure of liquidity – if and when priced into EGBs – is likely to change the way we price both the absolute level as well as the term structure of nominal yields… the discounts to the liquid asset are an increasing function of time to maturity and implied volatility… the term structure of liquidity also suggests that all else equal a longer-term cash flow bears a higher liquidity risk and hence requires a higher compensation in terms of discount relative a shorter-term cash flows.”