Citi equity research investigates the relation between currencies and equity markets. It suggests that typically large currency appreciation (depreciation) coincides with underperformance (outperformance) of the equity market in local currency terms. However, the currency moves tend to be larger than the equity moves. This supports the case for hedging local-currency equity exposure against currency strength and USD-based equity exposure against currency weakness. Hedge ratios should be diverse across countries, as correlation with currency weakness is a function of industry structure. Emerging market equities have historically not always correlated negatively with currencies due to the prevalence of crisis events.

“FX Illusion”, Citi Global Equities Strategy, February 27, 2013

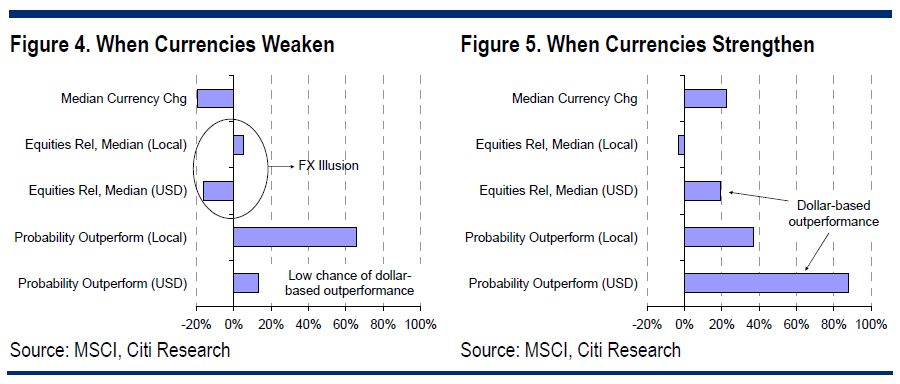

“The common perception is that a weaker currency is positive for the local economy and equity market… When a currency weakens, there are two effects that drive equity market performance. First, local EPS should rise, which can be because of translational effects (my US dollar profits is now worth more in Yen), or transactional (my costs are in Yen but I’m selling cars priced in dollars). Given the numerous layers of FX hedging companies undertake, we believe it is translational effects that are more important.”

“We studied more than 100 big FX depreciations around the world since 1990 and the effect a weaker currency had on respective equity performance. Our analysis included the major markets in both DM and EM when the local currency fell by 10% or more. The median currency fall in our sample was 19%. Almost always we found that the losses in the currency were greater than the outperformance, if any, of the local equity index. The median local currency outperformance during these periods of FX weakness was just 5% — less than the depreciation of the exchange rate. In only during 13% of these ‘big FX depreciations’ did a dollar-based investor outperform…We extended our analysis to look at periods of strengthening currencies. During these episodes, a dollar-based investor gains 22% on the currency but only loses 3% on local equity market relative performance….[In either direction] gains or losses in relative equity performance are usually dwarfed by losses or gains in the currency.”

“Markets which consistently come closest to offsetting FX weakness with stock price gains tend to have a concentration of exporters and multinationals with clear pricing power. They include Sweden, Germany, Switzerland, the US but not Japan.”

“In the 1990s, currency weakness in Emerging Markets was almost exclusively associated with crisis. Back then we had major devaluations in Asia and LatAm. Because of the crisis association, equity markets tended to perform poorly, especially for a dollar-based investor. The equity market and currencies fell together.”