On April 4 Bank of Japan Governor Haruhiko Kuroda unveiled aggressive “Quantitative and Qualitative Monetary Easing” (QQE), in order to meet a 2% inflation target within two years after 15 years of deflation. QQE means a shift of the operating targeting of the central bank to the monetary base, massive planned bond and other asset purchases, and a significant extension of duration in bond purchases. Market commentators almost uniformly concluded that QQE marks an extraordinary policy shift with historical dimensions and significant implication for global asset prices.

Haruhiko Kuroda, “Quantitative and Qualitative Monetary Easing” 12 April 2013,

http://www.boj.or.jp/en/announcements/press/koen_2013/ko130412a.htm/

(and various market research publications).

Background

“The Bank of Japan has engaged in a wide range of monetary easing efforts including the implementation of the zero interest rate policy, the quantitative easing policy, and comprehensive monetary easing…Despite its cumulative efforts, there have been no easily derived concrete results.”

“At the Monetary Policy Meeting held in January, the Bank set the price stability target at 2 percent in terms of the year on year rate of change in the consumer price index (CPI) and made a groundbreaking commitment to achieve that target at the earliest possible time…I have found it appropriate…to make a commitment with a time horizon of about two years…During the course of 15 years of deflation, the public’s behavior has been based on the assumption that prices would either decline or be unlikely to rise. It is necessary to eliminate deflationary expectations through the Bank’s strong commitment and intelligible explanation.”

“There is a reason to emphasize the qualitative aspect of monetary easing along with its quantitative aspect…The central banks’ purchases of government bonds and other assets from the markets have the effect of encouraging further declines in long-term interest rates and lowering risk premia of asset prices by absorbing risks – such as the one stemming from interest rate fluctuations. Consequently, it becomes important to determine not only how much liquidity to supply but also how to supply that quantity. ”

Measures

“The Monetary Policy Meeting on April 3 and 4…decided to embark on the quantitative and qualitative monetary easing…

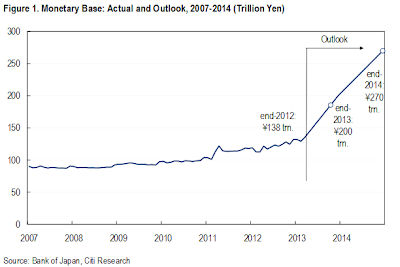

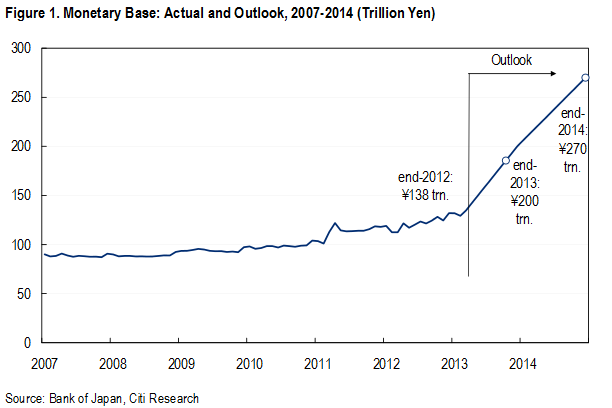

- The bank decided to change the main operating target for money market operations from the uncollateralized overnight call rate (i.e., interest rates) to the monetary base (i.e., quantity) and conduct money market operations so that the monetary base will increase at an annual pace of about 60–70 trillion yen [10-12% of GDP]… As of end-2012, its amount outstanding was 138 trillion yen, and it is expected to reach about 200 trillion yen at end-2013 and 270 trillion yen at end-2014. It will almost double in two years…

- As a means to increase the monetary base, the Bank decided to purchase JGBs so that its holding of their amount outstanding on the Bank’ s balance sheet will increase at an annual pace of about 50 trillion yen. Consequently, the Bank’s holding of JGBs will be increased from 89 trillion yen at end-2012 to 190 trillion yen at end-2014 [by about 17% of GDP]…

- In terms of quality, in increasing the purchases of JGBs, those with all maturities including 40-year bonds will be made eligible for purchase, and the average remaining maturity of the Bank’s JGB purchases will be extended from slightly less than three years at present to about seven years– equivalent to the average maturity of the amount outstanding of JGBs issued…

- Furthermore, with a view to lowering risk premia of asset prices, the Bank will purchase ETFs and Japan real estate investment trusts (J-REITs) so that their amounts outstanding on the Bank’s balance sheet will increase at an annual pace of about 1 trillion yen and about 30 billion yen, respectively [together less than 0.2% of GDP].”

Other principles

“Obviously, there will be both upside and downside risks to economic activity and prices going forward. The Bank will examine those risks carefully and will not hesitate to make adjustments as appropriate, should circumstances warrant.”

“The Bank does not believe 2 percent inflation achieved at a certain point in time is enough; rather, it believes 2 percent inflation should be maintained in a stable manner. Therefore, even if the inflation rate hits 2 percent at some point, the Bank could continue with the quantitative and qualitative monetary easing if it is judged necessary to do so in order to maintain that rate in a stable manner.”

“In order to avoid a possible arousal of doubt regarding the Bank’s increasing purchases of JGBs as financing fiscal deficits, it is vital for the government to clearly show the future course of fiscal consolidation and steadily make progress to reform the fiscal structure. On this point, the government –in the joint statement released with the Bank in January–stated that ‘in strengthening coordination between the Government and the Bank of Japan, the Government will steadily promote measures aimed at establishing a sustainable fiscal structure with a view to ensuring the credibility of fiscal management.’ We strongly expect the government to move on that front.”

Comments of market economists

State Street’s Michael Metcalf noticed: “The Fed’s first QE announcement had a dramatic impact on investor sentiment globally. The BoJ’s easing is 30% bigger in absolute terms, and relative to GDP is 3.5 times bigger…[A] modest areas for disappointment could be the breakdown of asset purchases themselves. The majority of the purchases will be in JGBs and an increase in the direct lending facility. Purchases of corporate bonds and ETFs were left largely unchanged from the asset purchases programme.”

According to J.P. Morgan’s Nikolaos Panigirtzoglou, “central bank purchases more than offset government bond supply [in 2013]. The BoJ is going to surpass government debt supply this year by buying USD720bn of government debt versus government net supply of USD320bn, resulting in a net withdrawal of USD400bn of government debt securities from bond markets [about 7% of GDP]”.

Standard Chartered’s Betty Rui Wangd and David Mann commented “The BoJ’s latest move is aggressive even compared to post-crisis actions by the Bank of England, the European Central Bank and the US Federal Reserve, and takes its policy further into uncharted territory…While the BoJ’s new easing policy is a step in the right direction, a growth strategy and a fiscal consolidation plan are needed to stabilise Japan‟s fundamentals and contain the risks created by easy money”

Bank of America/Merrill Lunch’s Michael Hartnett called Japan’s new monetary policy “Abe’s Bubble Economics” and concluded: “Just as Margaret Thatcher, Reagan and Volcker waged a successful War against Inflation in the early-1980s, Abe (and Kuroda and Bernanke) are waging a War against Deflation today. Abe wants the Nikkei to soar and JGB yields to collapse…The plan is more powerful than the BoJ’s policy ease in the early 2000s (ZIRP, QE via excess reserve targeting and purchases of long bonds, inflation target above zero for a few months, dollar purchase program, bank recapitalizations). The TOPIX more than doubled from 2003 to 2006 in response to the BoJ’s policies. Today, Japanese equities are cheaper, dividend yields are higher, and JGB yields are lower than they were in 2003”.