Standard & Poor’s research suggests that Japanese banks’ government bond holdings and interest rate risks of have almost doubled over the past 10 years. Against the backdrop of more aggressive reflation policies (view here) this translates into a systemic risk. An increase in long-term yields by 200bps compared to 2012 could already impair the banking system. An increase by 300bps or more could spell broadly based challenges for capital adequacy. A concurrent drop in equity would increase the pressure.

What Is The Japanese Banking System’s Tolerance For Rising Interest Rates?

Naoko Nemoto, Ryo Onodera, Standard & Poor’s ratings Service, July 8, 2013

http://www.standardandpoors.com/products-services/RatingsDirect-Global-Credit-Portal/en/us

“Standard & Poor’s Ratings Services expects long-term interest rates in Japan to rise as the country pushes to defeat deflation…Given a gradual increase in the outstanding balance of bonds that Japanese financial institutions hold, we view that interest rate risk for the banking system will likely surge.”

Banks interest rate risk has almost doubled over the past decade

“One thing Japanese banks all have in common is that they hold JGBs [Japanese Government Bonds]. This makes them susceptible to fluctuations in bond prices, and increases the likelihood of risk spreading among banks…The volume of interest rate risk has increased [over the past 10 years]. For instance, the amount of domestic bond holdings of city banks increased 2.4x from March 2003, and those of regional banks and shinkin banks (credit cooperatives) grew 1.6x…The ratio of the changes in bond prices under the assumption of a 100 basis point parallel shift in interest rates to net operating profit [at] city banks increased 1.5x and [at] regional financial institutions rose around 2x.

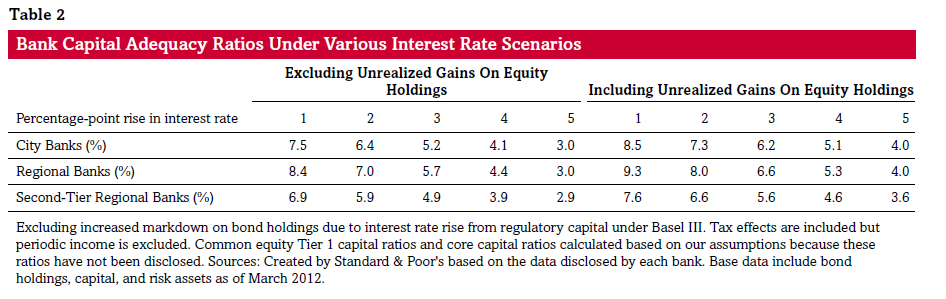

Falling bond prices would be very consequential for capital adequacy

“We define financial instability simply as banks having difficulty achieving their regulatory capital adequacy ratios. Currently, most regional banks…apply domestic standards… Unless market value falls by more than 30%, requiring impairment losses to be recognized, a bank’s regulatory capital would not decline due to the change in unrealized gains in [equity] securities…The recent stock price rally has boosted unrealized gains on equity held by the banks. Accordingly, if stock prices remain at levels as of March 2013, the unrealized gains are likely to partially offset any markdown on bond holdings caused by higher interest rates…Nevertheless, if a decline in portfolio values erodes banks’ capital, the confidence of investors and depositors may decline…In addition, if a bank needs to sell its bonds before maturity for some reason, it may have to recognize impairment losses. In consideration of these circumstances, we calculated the impact of interest rate increases by taking into account the impairment losses of banks applying domestic standards.”

“Japanese financial institutions are able to tolerate, in our view, an around 3 percentage-point rise in interest rates from the levels as of 2012, if we take their unrealized gains on equity holdings into account… To maintain the capital ratio of 5.5% including a 1% buffer, the rises in interest rates they can bear are 3.6 points for the city banks, 3.8 points for the regional banks, and 2.8 points for the second-tier regional banks, at a maximum.”

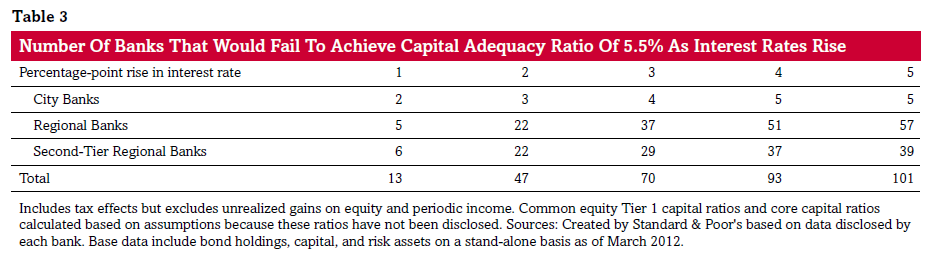

“We see a major gap in the banks’ tolerance for an interest rate rise by their amount of bond holdings and capital ratios. [The table below] shows the number of banks that would fail to achieve the capital ratio of 5.5% that includes a 1% buffer, if interest rates increase. If interest rates rise 2 percentage points, about 40% or 47 banks of a total of 112 city and regional banks…would fail to reach their required capital levels. If interest rates rise 3 percentage points, approximately 60%, or 70 banks, would fail. If unrealized gains are taken into account, the number of the banks that fail would fall to 32 in the case of the 2 point rise and 63 in the case of the 3 point rise. During the banking crisis in Japan in the late 1990s, even though the banking industry as a whole maintained regulatory capital levels, a group of weak banks emerged, undermining confidence in the entire system. Standard & Poor’s believes even a 2 percentage point rise in interest rates has the potential to affect the entire banking system.”

Other considerations

“In a sharp upward trend in interest rates, financial institutions would, of course, be cautious about purchasing JGBs. As of Sept. 30, 2012, financial institutions made up 64% of the private investors that hold JGBs. If the banks reduce their purchases of JGBs, the volatility risk of bond prices would increase due to lower liquidity in the market. If financial institutions’ capital shortage escalates, it would negatively affect the credit quality of the sovereign, as was the case in the European debt crisis.”

“The impact of an interest rate increase differs according to the economic circumstances. For instance, if the interest rate rise boosts the economic recovery, the potential loan growth, interest margin improvement, and lower credit costs would mitigate the negative impact of the rise. Nevertheless, we consider that profits may not improve as expected based on the following: replacement of portfolio components and improvement in yields take time; lending margins are subject to trends in short-term money market rates, as well as the financial standing and competitive environment of corporations; and although a large amount of demand deposits in a zero-interest rate environment are generally regarded as having low interest-rate sensitivity, if rates rise, a flight to term deposits from ordinary deposits could occur, which may lift funding costs.”