An academic summary paper shows how the structure of commodity markets has changed, most notably through the growth of commodity index investors. This has raised the correlation of commodities with other asset classes. Moreover, this financialization may impair at times the two key functions of commodity markets: risk sharing and price discovery.

“The Financialization of Commodity Markets”, Ing-Haw Cheng and Wei Xiong

Working Paper, October 2013

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2350243

The below are excerpts from the paper. Emphasis and cursive text has been added.

“Over the last decade, commodity futures have become a popular asset class for portfolio investors, just like stocks and bonds. This process is sometimes referred to as the financialization of commodity markets… This high price volatility has led to growing concern of the public and in policy circles as to whether financialization has distorted commodity prices, and whether more government regulation in these markets is warranted.”

How commodity markets have changed

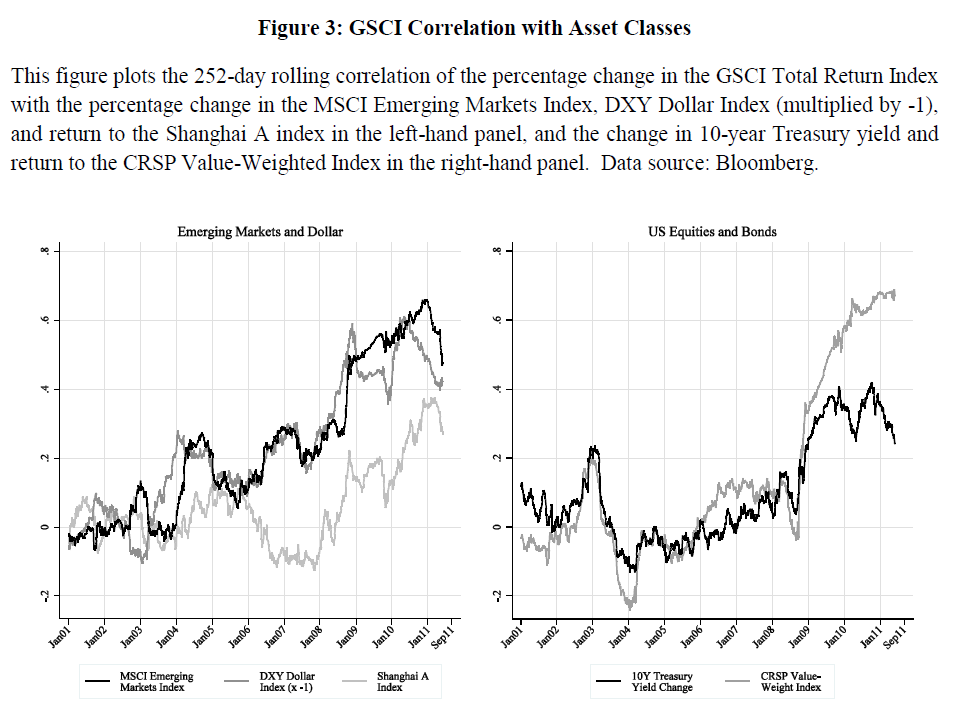

“Commodity futures prices have experienced a boom-bust cycle [from 2000 to 2011]… In searching for explanations for this pronounced ‘super-cycle’…researchers have noted that commodity futures price dynamics have changed substantially since 2000 and in particular since the financial crisis… Broadly, correlations [of commodities with other asset classes] trended upward from 2004-2008 and have increased significantly since the collapse of Lehman Brothers in 2008. Since then, they have stayed at elevated levels compared with historical periods.”

“The composition of participants in commodity futures markets has also dramatically changed over the past decade. Traditionally, researchers have viewed commercial hedgers and non-commercial traders (such as hedge funds) as the two major classes of market participants. Commercial hedgers such as farmers, producers, and consumers regularly trade commodity futures to hedge spot-price risk inherent in their commercial activities. Non-commercial traders, such as hedge funds or other managed money vehicles, invest others’ money on a discretionary basis in commodities, commodity futures, and options on futures, and make extensive use of leverage.”

“Over the past decade, there has been a large inflow of investment capital from a class of investors, so-called commodity index investors (CITs), also known as index speculators. CITs seek exposure to commodity prices as part of a broader portfolio strategy. They treat commodity futures as an asset class just like stocks and bonds, and often invest in instruments linked to broad-based indices such as the GSCI. On a practical level, CITs often establish commodity index positions by acquiring index swap contracts from financial swap dealers, or purchasing ETFs and ETNs.”

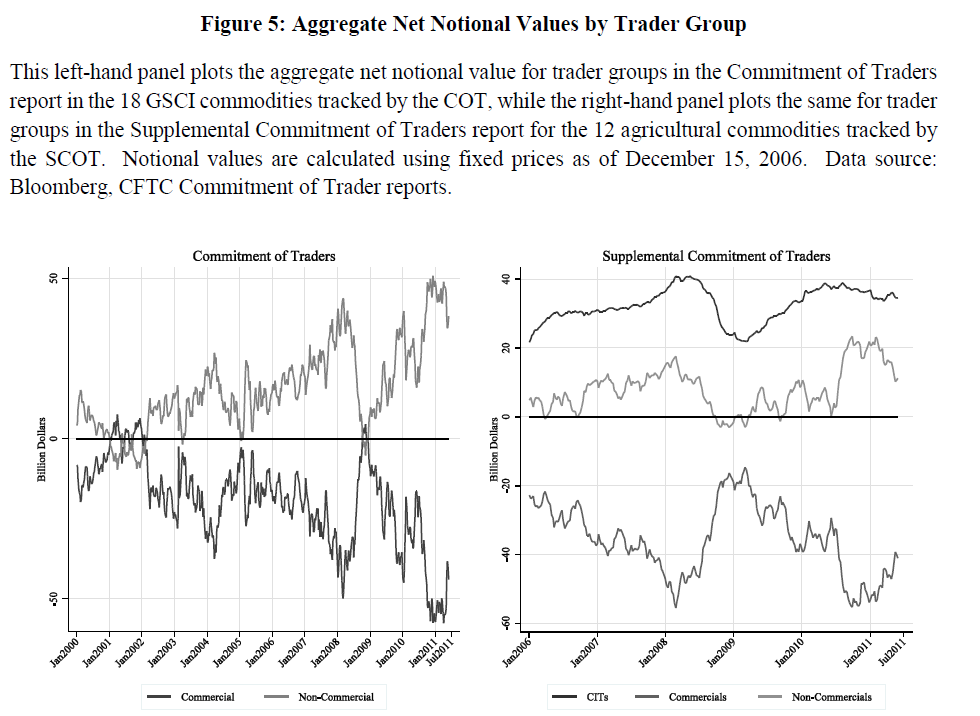

“The influx of CITs has led to significant changes in futures markets across two significant dimensions.

- First, gross positions in futures markets grew dramatically from 2004 through 2006. Data from the CFTC’s Commitment of Traders (COT)…shows that open interest in many commodities rose dramatically from 2004 onward.

- Second, although market-clearing implies that the net exposure of CITs, hedge funds, or commercial hedgers need not have grown as a result of the growth in gross positions, net exposures [across groups] did grow substantially, leading to the so-called financialization of futures markets…the growth in CIT investing has resulted in a dramatic expansion of the long side of agricultural futures markets.”

How financialization affects commodity markets

“Researchers should test whether financialization has affected commodity markets through the mechanisms that underpin [their] functioning…storage, risk-sharing, and information discovery….The evidence suggests that financialization may have transformed the latter two functions of commodity futures markets.”

Risk sharing

“Commodity futures markets have had a long history of assisting commodity producers to hedge their commodity price risks. The longstanding hedging pressure theory…posits that hedgers are typically on the short side of futures markets and need to offer positive risk premia to attract speculators to take the long side. By bringing a large number of financial investors to the long side, financialization mitigates this hedging pressure and improves risk sharing… Such risk premia, all else being equal, cause commodity futures curves to tilt towards backwardation. For this reason, this theory is also called the theory of normal backwardation…”

“Financial investors also have time-varying risk appetites owing to risk constraints and financial distress. For example, financial investors may have to unwind their long commodity positions if sudden price drops in other markets lead them to reduce risk. As a result, they transmit outside shocks to commodity markets. Financialization thus affects risk sharing in commodity markets through the dual roles of financial investors: as providers of liquidity to hedgers when trading to accommodate hedging needs and as consumers of liquidity from hedgers when trading for their own needs.”

Price discovery

“Financialization may also affect information discovery in commodity markets…centralized futures markets supplement commonly decentralized spot markets in information discovery… the futures prices of key commodities such as crude oil, copper, and soybeans have been widely used as barometers of the global economy in recent years…noise brought by trading of financial investors in futures markets can feed back to the commodity demand of final-goods producers. The key friction is that goods producers cannot differentiate whether futures prices move due to financial investor trading or due to changes in global economic fundamentals.”

“Participants of commodity markets face severe informational frictions. …Aggregating…information[regarding the supply, demand, and inventory of these commodities] from different countries or regions is challenging. The statistics from emerging economies are often scarce and unreliable. The statistics from OECD countries, while more reliable, are often delayed and also subject to subsequent revisions. Information regarding the supply and inventory of oil is difficult to capture completely, as it incorporates both above-ground, below-ground, and ship-board supplies. The process of quoting spot prices has also arguably been subject to manipulation due to these informational frictions…Motivated by the pervasive informational frictions in commodity markets, Singleton (2012) argues that heterogeneous beliefs can lead market participants to engage in speculative trading against each other, which, in turn, may induce commodity futures prices to drift away from fundamental values, and result in price booms and busts. Furthermore, he documents economically and statistically significant effects of investor flows on oil futures prices and attributes these effects to risk or informational channels distinct from changes in convenience yield.”