A new BIS paper argues that the expansion of EM local-currency bond markets and foreign-currency EM corporate issuance have strengthened the link between local EM financial conditions and global bond yields. The consequences would be (i) increased dependence of emerging financial systems on developed countries’ non-conventional monetary policies, (ii) decreased effectiveness of local monetary policies, and (iii) new systemic risks.

“The global long-term interest rate, financial risks and policy choices in EMEs”, Philip Turner

BIS Working Paper No 441, February 2014

http://www.bis.org/publ/work441.htm

The below are excerpts from the paper. Cursive text and emphasis have been added.

“During the 2000s, many EM governments became able to issue – and to sell to non-residents – long-term debt denominated in their own currency rather than in dollars…[and] avoided the currency mismatch risks created by heavy dollar borrowing in previous decades…The proportion of government debt denominated in local currency now dwarfs that of denominated in foreign currency… World Bank estimates put total local currency debt – that is, private as well as government – in the emerging markets by the end of 2012, at USD9.1 trillion, compared with USD4.9 trillion at the end of 2008.”

“Local currency bond markets…have also grown longer in maturity, and they are now, most important, closely integrated with global bond markets. Foreign holdings of EM local currency bonds have risen – the World Bank estimates that non-residents now hold 26.6% or more of local currency bonds, compared with 12.7% in 2008. There is clear statistical evidence that, since 2005, EM local currency bond yields have moved closely with US yields – which was not the case earlier.”

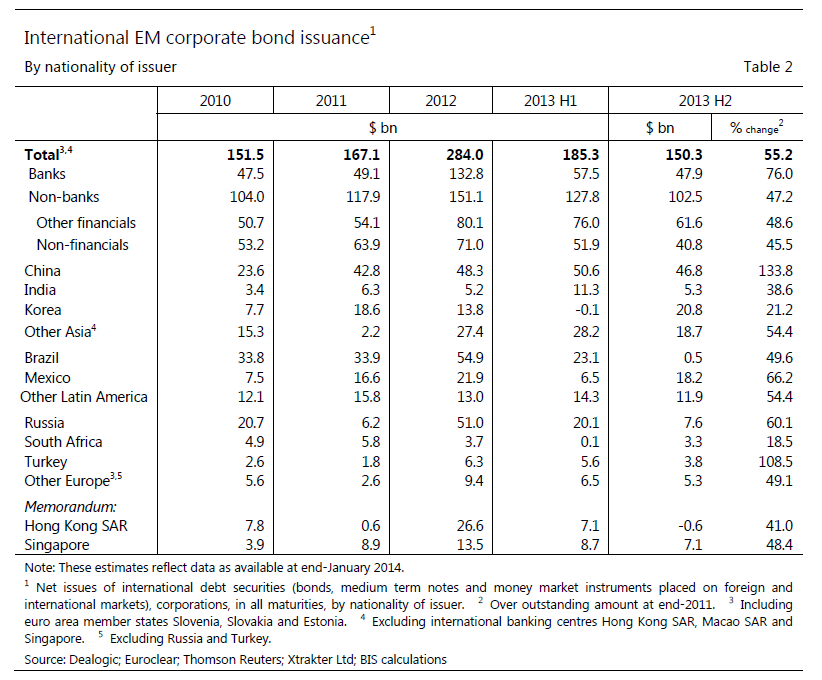

The rise of foreign-currency EM corporate issuance

“EM corporations – many of which could not easily issue in their home markets – have increasingly replaced EM sovereigns in international bond markets…EM borrowers have relied more on international bond markets and less on international banks…The massive expansion in EM corporate issuance in international bond markets in the past few years has probably increased forex risk exposures…[Evidence for this assertion includes that] there is no relation across countries between the increase in international bond issuance and the increase in exports.”

“Issuance by EM non-bank corporations on such a scale, and a possible “stop” at some point in the future, could affect the domestic banking systems in EMEs through at least three channels…

- When extremely easy external financing conditions allow such firms to borrow cheaply from abroad, local banks have to look for other customers…Domestic lending conditions…actually ease more than the expansion in total domestic bank credit aggregates suggest. A tightening in external financing conditions would reverse this…

- When EM corporations are awash with cash thanks to easy external financing conditions, they will increase their wholesale deposits with local banks. This is also reversible…

- If the local banks hedge their forex exposures with banks overseas, they still face the risk that local corporations will not be able to meet their side of the contract…The domestic bank that thinks it has managed its risks, will find itself, if its corporate clients fail, with unhedged exposures vis-à-vis foreign banks.”

Growing EM dependence on global interest rates

“The global long-term interest rate now matters much more for the monetary policy choices facing emerging market economies than a decade ago. The low or negative term premium in the yield curve in the advanced economies from mid-2010 has pushed international investors into EM local bond markets: by lowering local long rates, this has considerably eased monetary conditions in the emerging markets…These developments strengthen the feedback effects between bond and foreign exchange markets. They also have significant implications for local banking systems.”

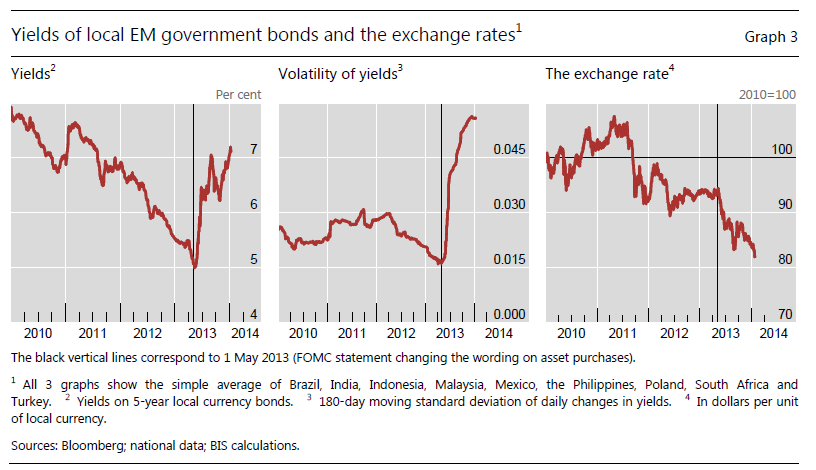

“Expectations about the exchange rate and the long-term interest rate are often jointly determined: expectations of currency depreciation, for instance, may also drive down the prices of local currency bonds. Such joint determination will be particularly evident after financial shocks – domestic or foreign. Graph 3 shows a simple average of movements in bond yields and in the exchange rate of several major EM economies. Long-term interest rates in major EM economies fell during 2011 and 2012. Then the FOMC statement of 1 May 2013 led bond markets worldwide to fall. Market volatility rose sharply. There was also a near simultaneous decline in the exchange rate of many EM currencies against the dollar.”

“Without capital controls, and assuming the country’s credit standing is constant, the long-term rate in the local currency will be heavily influenced by developments in dollar bond markets. There is a loss of independence irrespective of the country’s choice of exchange rate regime.”