A University of York paper suggests that equity strategies based on fundamentals and strategies based on momentum are complementary. Thus, relative momentum seems to be a useful overlay for earnings growth-oriented portfolios (probably detecting when high growth companies hit a snag). And trend following has historically reduced volatility and drawdowns of both value and growth strategies.

Care, Andrew, James Seaton, Peter Smith, and Stephen Thomas, (2014) “When Growth Beats Value: Removing Tail Risk from Global Equity Momentum Strategies”, University of York, Discussion Paper in Economics, 14/09.

http://www.york.ac.uk/media/economics/documents/discussionpapers/2014/1409.pdf

The below are excerpts from the paper. Emphasis and cursive text have been added.

A recap of basic equity investment styles

1. Value

“Metrics for individual stocks that help to identify value stocks have included dividend yield, total payout yield, and price-to-cashflow… the most widely known measure of value is a stock’s book-to-market ratio.”

According to MSCI, attributes for defining value stocks are [i] the book value to price ratio, [ii] the 12-month forward earnings to price ratio, and [iii] the dividend yield of a stock.

2. Growth

Growth stocks feature high expected earnings per share (EPS) growth. According to MSCI, attributes defining a growth stock are [i] the long-term forward EPS growth rate, [ii] the short-term EPS growth rate, [iii] the current internal growth rate, [iv] the long-term historical EPS growth rate, and [vi] the long-term historical sales per share growth trend.

3. Relative momentum

“[A popular strategy in the equity space is] cross-sectional, or relative momentum, where portfolios are generally formed with a fixed amount of long and short positions each month irrespective of how the aggregate market is performing…An adjustment to this strategy…involves volatility-adjusting the past return to avoid the most volatile assets appearing disproportionately often in high and low momentum categories.”

4. Trend following

“The second type of momentum strategy… has been widely known as ‘trend following’ and is an approach frequently used by Commodity Trading Advisors (CTAs). In this type…one is interested in the absolute direction of an asset’s price rather than how one asset has performed relative to another. This could be based on whether the asset has shown a positive excess return over the past 12-months,, whether the excess return has been positive over a range of time frames, or whether the current price is in excess of a moving average, or on other similar metrics.”

The empirical research

“In this paper we… explore the interaction between value and growth investing on the one hand and both absolute and relative momentum on the other… we apply our analysis to MSCI indices of value and growth for both developed economy and emerging economy stock markets.”

“This study utilizes MSCI Value and Growth equity indices for 23 developed and 21 emerging countries… The developed economy indices begin in December 1974, while the emerging market indices start in December 1996 [with exceptions]. [The sample period goes to 2012].”

The empirical findings

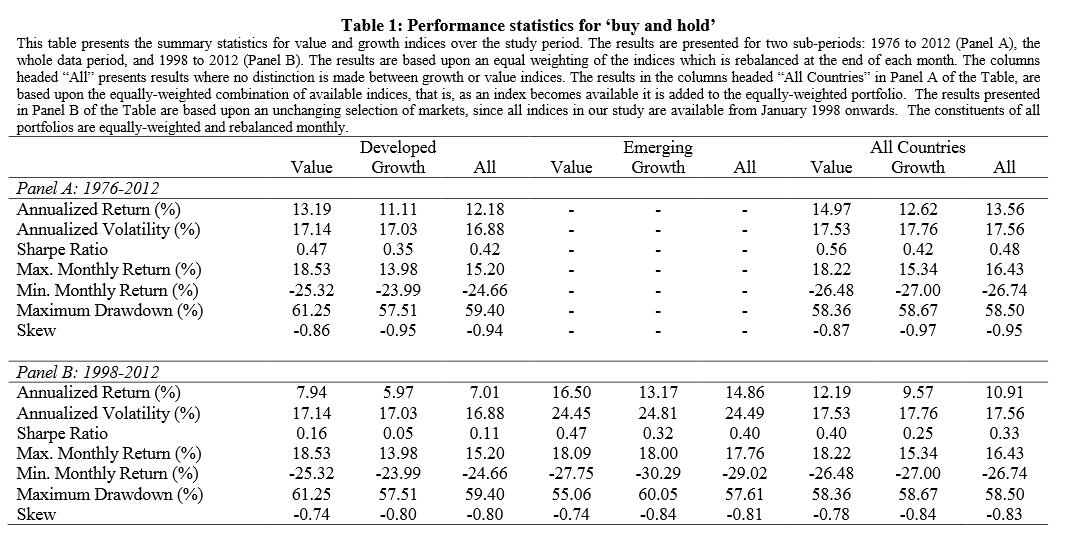

“Any investor…in an equally weighted portfolio of the indices would have experienced significant drawdowns over the sample period, with returns being both volatile and negatively skewed.”

“[Our research] confirms the conventional finding that value stocks tends to outperform growth stocks across all periods and in the case of both developed and emerging markets. Returns are typically 2-3% higher per year for value indices while volatilities are fairly similar for both strategies…The outperformance of value stocks over growth stocks has been a well-documented phenomenon in the finance literature. When we create portfolios using the relative momentum filter we find that returns are enhanced by the filter. However, the drawdowns, the high volatility in returns and negative skewness remain as a feature of the performance.”

“The most significant aspect of our results however, relates to the way in which the relative momentum and trend following filters affects the value and growth portfolios…

- In terms of the interaction between relative momentum and investment style (value or growth), we observe that the Sharpe ratios remain fairly similar in developed value portfolios regardless of how momentum is introduced (top 5, or top 25%). Emerging value portfolios have lower Sharpe ratios with the introduction of a relative momentum filter. The big gains from the use of relative momentum seem to accrue in the growth portfolios. For developed growth portfolios, returns increase by around 5 to 7% per annum with only slight increases in volatility…The Sharpe ratios of these growth portfolios are now higher than those of comparable value portfolios…

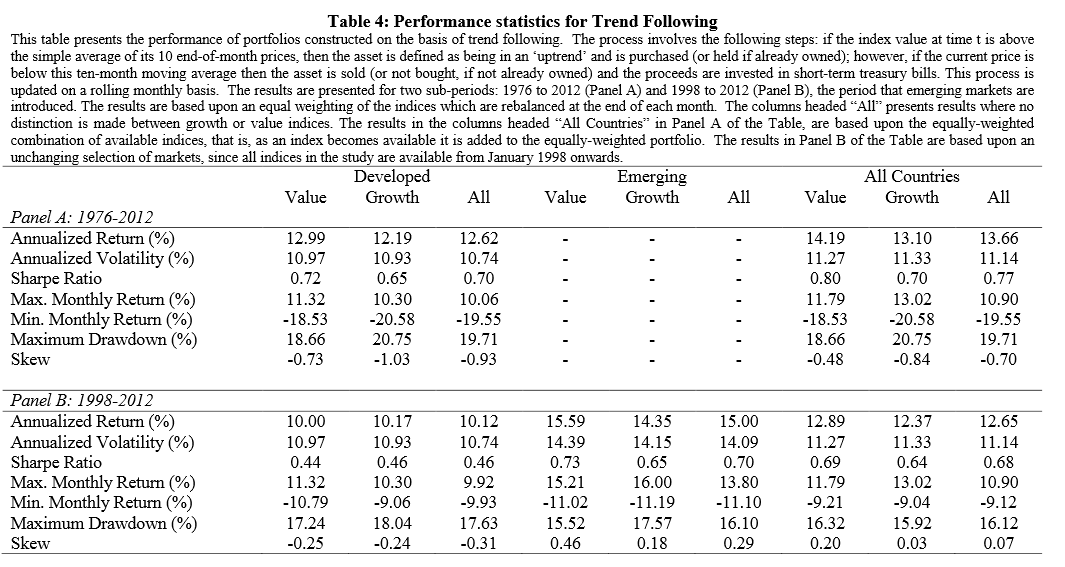

- [The table below] reports the results of [the impact of] trend following on value and growth portfolios…The major difference…relates to volatility and maximum drawdowns. With trend following annualised volatility falls to around 11% compared to around 17%….Perhaps most significantly for ordinary investors, the maximum drawdown statistics for this 36-year period fall from around 55% to 60% to around 20%. The results are fairly similar regardless of whether value, growth or a combination of the two are held in portfolios…One of the most appealing characteristics of trend following…appears to be the ability to substantially reduce drawdowns by being invested in T-Bills during major bear markets…”

“We find that in many cases the risk-adjusted outperformance of value over growth investing disappears, particular when the trend following filter is used and, in some cases, the performance advantage actually reverses.”

A thought on the interaction of investment styles

“While value and momentum are well established investment strategies, there has been less attention focused on the interaction between the two. For a stock to become cheap on a value metric it needs the fundamentals to improve relative to the price. In the case of an earnings yield (E/P) approach, this means that E needs to increase (decrease) at a faster (slower) rate than P rises (falls). …[This also implies that in case of large price shocks the two metrics usually move in opposite directions]…In the cases where P falls this makes it less likely the stock will qualify as a cross-sectional momentum winner and almost certainly rules it out from having positive absolute momentum.”