Since 2008, Bank delevering has been on of the key drivers of the euro areas poor economic performance and its vulnerability to recurrent financial crises. Barclays Cross Asset Research nicely summarized and discussed its main drivers, whose impact is widely seen as most intense in 2012 and maybe 2013. ECB and IMF research suggests that the deleveraging is ongoing and could eventually reach an equivalent of 10-30% of euro area GDP.

Sources: Bank Deleveraging in Europe: Not done yet, Barclays Capital, 11 October 2012;

ECB Financial Stability Review, June 2012

IMF Global Financial Stability Report, October 2012

According to Barclays, ”this restructuring process, which has been ongoing for over three years, is more than two-thirds complete, although further non-core run-off will occur.”

The second trigger was the European Banking Authority’s September 2011 exercise to determine if banks had enough capital when market prices of government bonds were considered. Banks were allowed to meet identified capital needs by either raising equity or reducing risk-weighted assets, and many did both. Banks in this category include Santander, BBVA, and Unicredit. Specifically, the European Banking Authority had identified a EUR115bn capital requirement at European banks, basing the assessment on a 9% core tier 1 ratio after adjustments for sovereign risk holdings. Banks that were calculated to have a capital shortfall, of which there were 37, had until 30 June 2012 to implement a capital raising plan. The actions largely focused on retaining earnings, liability management, conversions of non-qualifying capital instruments, or rights issues, but, there was also a significant component of balance sheet reduction. According to Barclays, this process had been complete by October 2012.

The third trigger was the looming requirements of Basel 3, which are particularly onerous on banks with large fixed income trading operations. There are two things to consider when thinking about the deleveraging occurring in response to Basel 3. The first is banks – particularly investment banks – shrinking their balance sheets in response to the enhanced recognition of counterparty risk in Basel 3 that leads to RWA inflation in fixed income trading businesses. The primary examples of banks responding to this with deleveraging are Credit Suisse and UBS. The second is banks shrinking their assets to improve their Basel 3 capital ratios faster in response to market and regulatory pressure.

Implementation of Basel 3 is scheduled to begin on January 1, 2013. While the deductions linked to qualifying capital and the transition periods for minimum ratios phase in slowly, the adjustments to risk-weighted asset calculations occur instantaneously. The phase-in period for many deductions and for higher minimum capital requirements is long, with full implementation not scheduled until 2018. Part of the rationale for this long phase-in period is to prevent unnecessary deleveraging of the banking system. Despite this, the market and regulators have been increasingly focusing on banks’ ‘fully loaded’ Basel 3 ratios, calculated as if the full standard was applied currently. On a fully loaded Basel 3 basis many banks are thinly capitalized, with ratios below the 8% that the market considers appropriate. For example, dealer inventories of fixed income assets have been plummeting, as shown below in primary dealer inventories of corporate bonds that have fallen 50% between 2011 and 2012.

According to Barclays, “banks with capital markets operations have deleveraged in anticipation of more onerous risk-weighted asset calculations under Basel 3…but Basel 3-relate deleveraging [is] to spread as banks face pressure from investors and regulators to achieve higher fully loaded Basel 3 capital ratios sooner.”

The fourth and final trigger of deleveraging were funding challenges, namely the withdrawal of USD liquidity from money market funds to European banks led BNP, Societe Generale, and Credit Agricole to announce deleveraging plans focused on reducing assets funded in USD. In 2011, almost 50% of all assets in US prime money market funds were invested in European banks. As the European debt crisis escalated in the second half of 2011, this concentration became a concern, and money market funds reacted by withdrawing some of their liquidity provision To facilitate this withdrawal in an orderly fashion, the ECB, in conjunction with other central banks, increased its provision of USD funding.We believe broader changes in the funding market, such as the elevated cost and reduced availability of unsecured debt, would have caused significantly more deleveraging if not for the exceptional liquidity being provided by the ECB.

-

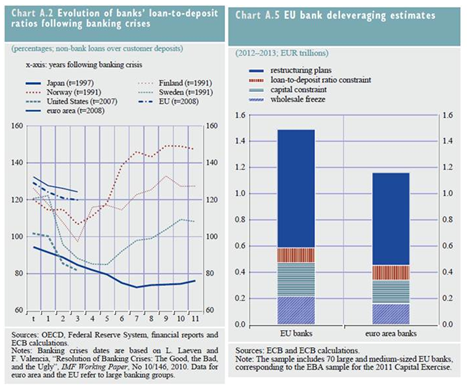

Capital constraints: banks facing a capital shortfall at the end of 2013 under a macroeconomic scenario contingent on the European Commission’s Spring 2012 Forecast that affects the amount of their loan losses and their net operating income, and assuming the core Tier 1 capital ratio threshold of 9%, may decide to reduce their risk-weighted assets, instead of raising fresh capital in the markets, to close the gap. The estimated capital shortfall is mitigated by the capital accumulated in the context of the EBA’s 2011 EU Capital Exercise (to be completed by the end of June 2012) and by the potential beneficial impact on banks’ earnings of the two three-year LTROs conducted by the Eurosystem in December 2011and February 2012.

- Wholesale funding constraints: banks may not be able to roll over all their maturing wholesale funding over the two-year horizon It has been assumed that banks will roll over only 90% of their wholesale debt maturing in 2012 and 2013. The funding constraints will, however, be mitigated by the substantial net take-up of the two three-year LTROs.

- Structural funding constraints: in addition, some deleveraging needs may arise on account of structural funding pressures that reflect banks’ incentives to reduce their reliance on short-term, volatile funding sources. Against this background, country-specific targets for banks’ loan-to-deposit ratios were imposed. Those targets are largely based on the assumptions of the EU/International Monetary Fund (IMF) adjustment programs.

The IMF estimates that large EU banks would reduce assets by USD2200-3800 billion (12-21% of EU GDP) from 2011Q3 to 2013Q4. Indeed, assets fell by more than USD600 billion in the period from 2011Q3 to 2012Q2 (3-3.5% of GDP) with much of the decline occurring in 2011Q4. Since then, following efforts by the ECB to relieve funding pressures, the pace of deleveraging has slowed. To date, the decline in bank leverage has been mainly due to capital measures and asset disposals; cutbacks in bank loans have played a smaller role.