A Nomura research report looks at the rising financial risk premium across Asia. It shows that economic fundamentals are not as bad as they were in 1996. However, Asia’s external surplus has been eroded by a torrid financial expansion, which was fueled by very easy monetary policy. In the absence of a correction of this policy stance, there is an increasing danger that capital outflows will trigger a sudden stop to these accommodative financial conditions.

Asia’s rising risk premium

Nomura Global Markets Research – June 2013

Full report is proprietary research of Nomura Global Markets. Please contact for access.

Deteriorating external balances as consequence of soaring financial leverage

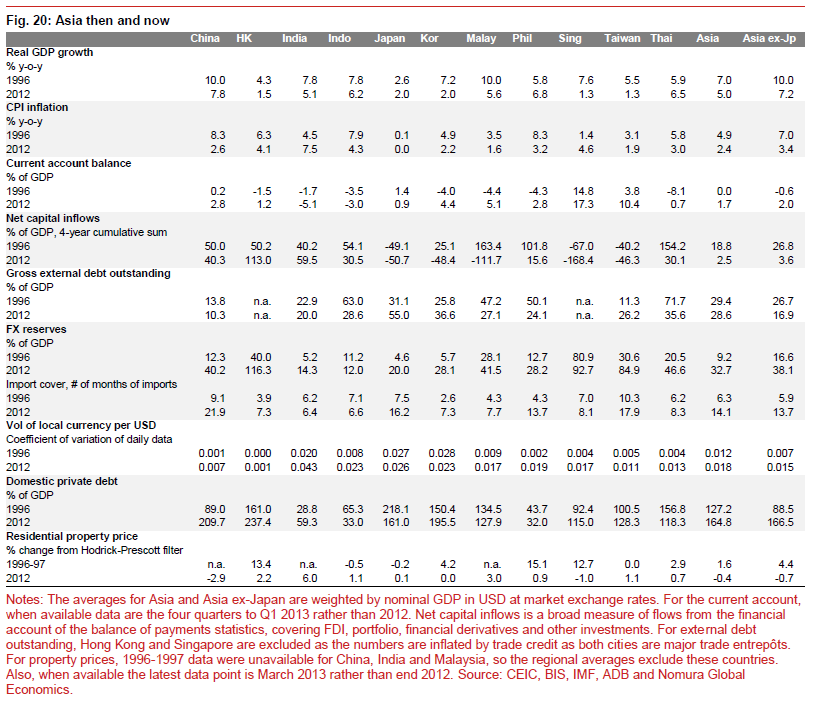

“Asia’s current account trend has undergone a dramatic change since the global financial crisis. On a four-quarter rolling sum basis, the Asia 11’s surplus has narrowed from a peak of USD726bn (6.3% of GDP) in Q3 2007 to USD327bn, (1.6% of GDP) in Q4 2012, the smallest surplus recorded since the Asian crisis in Q4 1997.”

“From the peak in 2007 to Q1 2013, current account surpluses have narrowed by more than 13pp of GDP in Hong Kong, Malaysia and Singapore and by 8-9pp of GDP in China, India and Thailand. The sharp narrowing swung the current accounts of India and Indonesia into deficits of 3.6% of GDP and 2.4% of GDP, respectively, in Q1 2013.”

“The narrowing of China’s current account surplus from 10.1% of GDP in 2007 to 2.3% of GDP in 2012 can be 83% explained by the surge in gross domestic investment from 41.6% of GDP in 2007 to 48.1% of GDP in 2012…In India and Indonesia, the swing to deficits has more to do with a lack of reforms causing domestic supply-side bottlenecks and crimping domestic savings. In other countries, the narrowing surpluses are chiefly a result of insufficient saving, which reflects the rapid build-up of debt.”

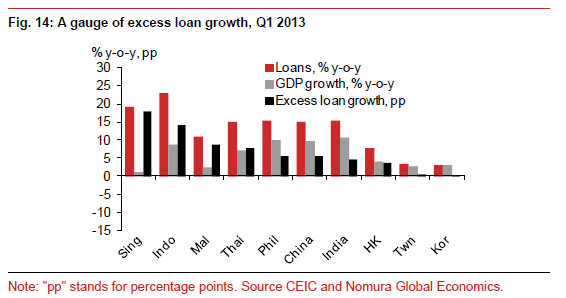

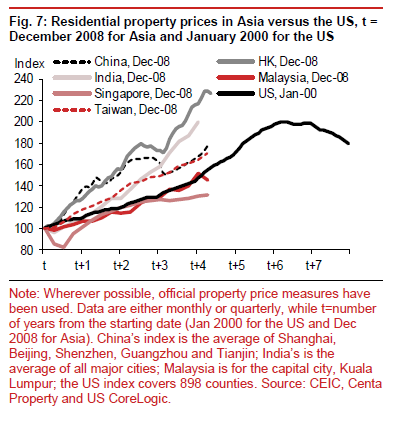

“Asia’s average ratio of domestic private debt to GDP was 167% in 2012, significantly higher than in 1996 – and the property markets in most of these countries are frothy. It is not only the level of leverage, but also the speed of the buildup. In the four years since the global financial crisis, the ratio of private domestic debt to GDP has increased by over 50 percentage points (pp) of GDP in Hong Kong and Singapore, and between 30-40pp in Malaysia, Korea, China and Thailand. Based on the latest available data, domestic private credit is continuing to outpace nominal GDP in all countries but Korea.”

“Monetary policy is even looser once the stage of the financial cycle is taken into account. We measure the financial cycle for each country by combining domestic private credit and property prices. The financial cycles in most countries are currently above trend and out of sync with the business cycle.”

“Asia has come to rely increasingly on macroprudential tools in its attempts to contain credit and property market booms. But macroprudential tools are not the Holy Grail. These tools risk lulling central banks into a false sense of believing that policy has been sufficiently tightened only to find out that, over time, as loopholes are found, these tools have turned out to be a poor substitute for higher interest rates.”

Comparison to the 1990s Asian Crisis

“While Asia’s economic fundamentals have deteriorated since the global financial crisis, they are still much better than in 1996, but comparisons to 1996 may not be valid. To avoid future crises, the time to arrest the slide in the region’s fundamentals is now. As explained in the next section, this will require a move away from ultra-loose counter-cyclical policies and an increased focus on structural reforms. The one strong conclusion from this comparison is that, with the possible exceptions of India and Indonesia, balance of payments crises are much less likely, as Asia’s FX reserves are much larger than before the Asian crisis. Although, if remedial action is not taken soon, domestic financial crises in Asia will become more likely.”