Macro-quantamental indicators are time series of macroeconomic information states designed for the development and backtesting of financial markets trading strategies. They are the building blocks for the macro-quantamental technology, i.e., investment strategies based on the systematic use of macroeconomic information.

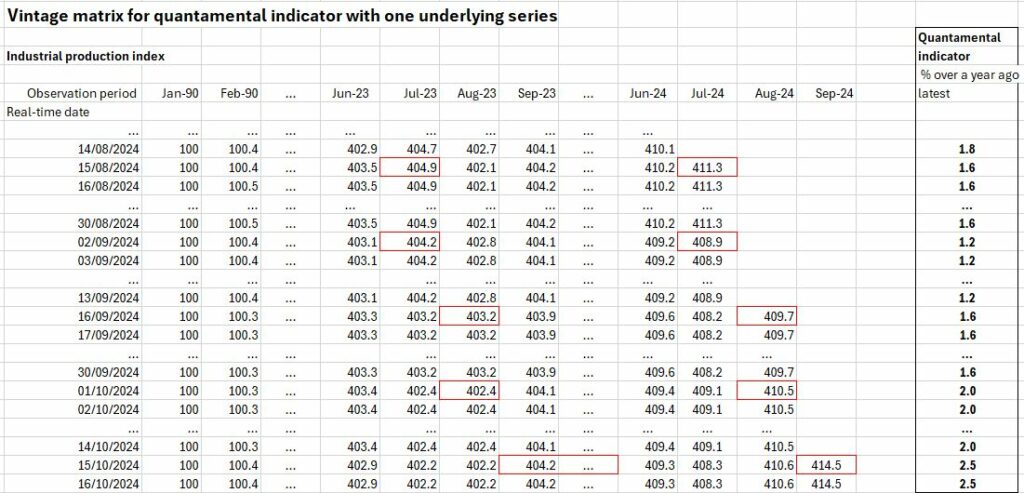

Example: Standard economic time series of production trends versus quantamental series

Example: Explanatory power of standard economic versus quantamental series

The key source of macro-quantamental information for institutional investors is the J.P. Morgan Macrosynergy Quantamental System or JPMaQS. It is a service that makes it easy to use quantitative-fundamental (“quantamental”) information for financial market trading. With JPMaQS, users can access a wide range of relevant macro-quantamental data that are designed for algorithmic strategies, as well as for backtesting macro trading principles in general.

The official documentation site of JPMaQS on J.P. Morgan Markets can be found here.